Hedgecraft Part 1: Building a Minimally Correlated Portfolio with Data Science¶

What is the optimal way of constructing a portfolio? A portfolio that (1) consistently generates wealth while minimizing potential lossess and (2) is robust against large market fluctuations and economic downturns? I will explore these questions in some depth in a three-part *Hedgecraft* series. While the series is aimed at a technical audience, my intentions are to break the technical concepts down into digestible bite-sized pieces suitable for a general audience, institutional investors, and others alike. The approach documented in this notebook (to my knowledge) is novel. To this end, the penultimate goal of the project is an end-to-end FinTech/Portfolio Management product.

Summary¶

Using insights from Network Science, we build a centrality-based risk model for generating portfolio asset weights. The model is trained with the daily prices of 31 stocks from 2006-2014 and validated in years 2015, 2016, and 2017. As a benchmark, we compare the model with a portolfio constructed with Modern Portfolio Theory (MPT). Our proposed asset allocation algorithm significantly outperformed both the DIJIA and S&P500 indexes in every validation year with an average annual return rate of 38.7%, a 18.85% annual volatility, a 1.95 Sharpe ratio, a -12.22% maximum drawdown, a return over maximum drawdown of 9.75, and a growth-risk-ratio of 4.32. In comparison, the MPT portfolio had a 9.64% average annual return rate, a 16.4% annual standard deviation, a Sharpe ratio of 0.47, a maximum drawdown of -20.32%, a return over maximum drawdown of 1.5, and a growth-risk-ratio of 0.69.

Background¶

In this series we play the part of an Investment Data Scientist at Bridgewater Associates performing a go/no go analysis on a new idea for risk-weighted asset allocation. Our aim is to develop a network-based model for generating asset weights such that the probability of losing money in any given year is minimized. We've heard down the grapevine that all go-descisions will be presented to Dalio's inner circle at the end of the week and will likely be subject to intense scrutiny. As such, we work with a few highly correlated assets with strict go/no go criteria. We build the model using the daily prices of each stock (with a few replacements*) in the Dow Jones Industrial Average (DJIA). If our recommended portfolio either (1) loses money in any year, (2) does not outperform the market every year, or (3) does not outperform the MPT portfolio---the decision is no go.

- We replaced Visa (V), DowDuPont (DWDP), and Walgreens (WBA) with three alpha generators: Google (GOOGL), Amazon (AMZN), and Altaba (AABA) and, for the sake of model building, one poor performing stock: General Electric (GE). The dataset is found on Kaggle.

Asset Diversification and Allocation¶

The building blocks of a portfolio are assets (resources with economic value expected to increase over time). Each asset belongs to one of seven primary asset classes: cash, equitiy, fixed income, commodities, real-estate, alternative assets, and more recently, digital (such as cryptocurrency and blockchain). Within each class are different asset types. For example: stocks, index funds, and equity mutual funds all belong to the equity class while gold, oil, and corn belong to the commodities class. An emerging consensus in the financial sector is this: a portfolio containing assets of many classes and types hedges against potential losses by increasing the number of revenue streams. In general the more diverse the portfolio the less likely it is to lose money. Take stocks for example. A diversified stock portfolio contains positions in multiple sectors. We call this asset diversification, or more simply diversification. Below is a table summarizing the asset classes and some of their respective types.

| Cash | Equity | Fixed Income | Commodities | Real-Estate | Alternative Assets | Digital | |

|---|---|---|---|---|---|---|---|

| US Dollar | US Stocks | US Bonds | Gold | REIT's | Structured Credit | Cryptocurrencies | |

| Japenese Yen | Foreign Stocks | Foreign Bonds | Oil | Commerical Properties | Liquidations | Security Tokens | |

| Chinese Yaun | Index Funds | Deposits | Wheat | Land | Aviation Assets | Online Stores | |

| UK Pound | Mutual Funds | Debentures | Corn | Industrial Properties | Collectables | Online Media | |

| • | • | • | • | • | • | • | |

| • | • | • | • | • | • | • |

An investor solves the following (asset allocation) problem: given X dollars and N assets find the best possible way of breaking X into N pieces. By "best possible" we mean maximizing our returns subject to minimizing the risk of our initial investment. In other words, we aim to consistently grow X irrespective of the overall state of the market. In what follows, we explore provocative insights by Ray Dalio and others on portfolio construction.

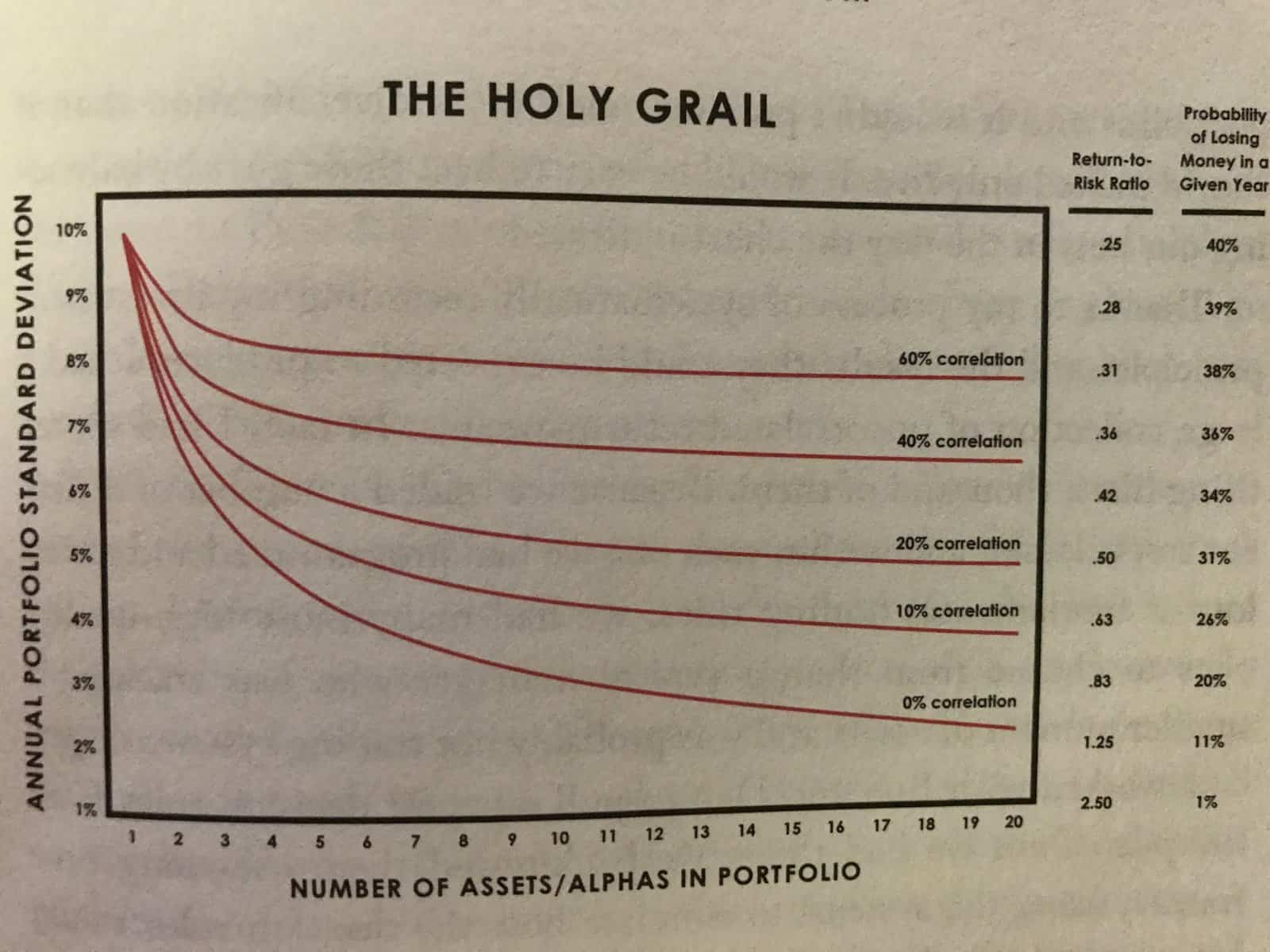

Source: Principles by Ray Dalio (Summary)

Source: Principles by Ray Dalio (Summary)

The above chart depicts the behaviour of a portfolio with increasing diversification. Along the x-axis is the number of asset types. Along the y-axis is how "spread out" the annual returns are. A lower annual standard deviation indicates smaller fluctuations in each revenue stream, and in turn a diminished risk exposure. The "Holy Grail" so to speak, is to (1) find the largest number of assets that are the least correlated and (2) allocate X dollars to those assets such that the probability of losing money any given year is minimized. The underlying principle is this: the portfolio most robust against large market fluctuations and economic downturns is a portfolio with assets that are the most independent of eachother.

Exploratory Data Analysis and Cleaning¶

Before we dive into the meat of our asset allocation model, we first explore, clean, and preprocess our historical price data for time-series analyses. In this section we complete the following.

- Observe how many rows and columns are in our dataset and what they mean.

- Observe the datatypes of the columns and update them if needed.

- Take note of how the data is structured and what preprocessing will be necessary for time-series analyses.

- Deal with any missing data accordingly.

- Rename the stock tickers to the company names for readability.

#import data manipulation (pandas) and numerical manipulation (numpy) modules

import pandas as pd

import numpy as np

#silence warnings

import warnings

warnings.filterwarnings("ignore")

#reads the csv file into pandas DataFrame

df = pd.read_csv("all_stocks_2006-01-01_to_2018-01-01.csv")

#prints first 5 rows of the DataFrame

df.head()

| Date | Open | High | Low | Close | Volume | Name | |

|---|---|---|---|---|---|---|---|

| 0 | 2006-01-03 | 77.76 | 79.35 | 77.24 | 79.11 | 3117200 | MMM |

| 1 | 2006-01-04 | 79.49 | 79.49 | 78.25 | 78.71 | 2558000 | MMM |

| 2 | 2006-01-05 | 78.41 | 78.65 | 77.56 | 77.99 | 2529500 | MMM |

| 3 | 2006-01-06 | 78.64 | 78.90 | 77.64 | 78.63 | 2479500 | MMM |

| 4 | 2006-01-09 | 78.50 | 79.83 | 78.46 | 79.02 | 1845600 | MMM |

Date: date (yyyy-mm-dd)Open: daily opening prices (USD)High: daily high prices (USD)Low: daily low prices (USD)Close: daily closing prices (USD)Volumedaily volume (number of shares traded)Name: ticker (abbreviates company name)

#prints last 5 rows

df.tail()

| Date | Open | High | Low | Close | Volume | Name | |

|---|---|---|---|---|---|---|---|

| 93607 | 2017-12-22 | 71.42 | 71.87 | 71.22 | 71.58 | 10979165 | AABA |

| 93608 | 2017-12-26 | 70.94 | 71.39 | 69.63 | 69.86 | 8542802 | AABA |

| 93609 | 2017-12-27 | 69.77 | 70.49 | 69.69 | 70.06 | 6345124 | AABA |

| 93610 | 2017-12-28 | 70.12 | 70.32 | 69.51 | 69.82 | 7556877 | AABA |

| 93611 | 2017-12-29 | 69.79 | 70.13 | 69.43 | 69.85 | 6613070 | AABA |

#prints information about the DataFrame

df.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 93612 entries, 0 to 93611 Data columns (total 7 columns): Date 93612 non-null object Open 93587 non-null float64 High 93602 non-null float64 Low 93592 non-null float64 Close 93612 non-null float64 Volume 93612 non-null int64 Name 93612 non-null object dtypes: float64(4), int64(1), object(2) memory usage: 5.0+ MB

Some observations:

- The dataset has 93,612 rows and 7 columns.

- The

Datecolumn is not a DateTime object (we need to change this). - For time-series analyses we need to preprocess the data (we address this in the proceeding section).

- There are missing values in the

Open,High, andLowcolumns (we adress this after preprocessing the data). - We also want to map the tickers (e.g., MMM) to the company names (e.g., 3M).

- Finally, we need to set the index as the date.

#changes Date column to a DateTime object

df['Date'] = pd.to_datetime(df['Date'])

#prints unique tickers in the Name column

print(df['Name'].unique())

['MMM' 'AXP' 'AAPL' 'BA' 'CAT' 'CVX' 'CSCO' 'KO' 'DIS' 'XOM' 'GE' 'GS' 'HD' 'IBM' 'INTC' 'JNJ' 'JPM' 'MCD' 'MRK' 'MSFT' 'NKE' 'PFE' 'PG' 'TRV' 'UTX' 'UNH' 'VZ' 'WMT' 'GOOGL' 'AMZN' 'AABA']

#dictionary of tickers and their respective company names

ticker_mapping = {'AABA':'Altaba',

'AAPL':'Apple',

'AMZN': 'Amazon',

'AXP':'American Express',

'BA':'Boeing',

'CAT':'Caterpillar',

'MMM':'3M',

'CVX':'Chevron',

'CSCO':'Cisco Systems',

'KO':'Coca-Cola',

'DIS':'Walt Disney',

'XOM':'Exxon Mobil',

'GE': 'General Electric',

'GS':'Goldman Sachs',

'HD': 'Home Depot',

'IBM': 'IBM',

'INTC': 'Intel',

'JNJ':'Johnson & Johnson',

'JPM':'JPMorgan Chase',

'MCD':'Mcdonald\'s',

'MRK':'Merk',

'MSFT':'Microsoft',

'NKE':'Nike',

'PFE':'Pfizer',

'PG':'Procter & Gamble',

'TRV':'Travelers',

'UTX':'United Technologies',

'UNH':'UnitedHealth',

'VZ':'Verizon',

'WMT':'Walmart',

'GOOGL':'Google'}

#changes the tickers in df to the company names

df['Name'] = df['Name'].map(ticker_mapping)

#sets the Date column as the index

df.set_index('Date', inplace=True)

Preprocessing for Time-Series Analysis¶

In this section we do the following.

- Break the data in two pieces: historical prices from 2006-2014 (

df_train) and from 2015-2017 (df_validate). We build our model portfolio using the former and test it with the latter.

2. We add a column to df_train recording the difference between the daily closing and opening prices Close_diff.

3. We create a seperate DataFrame for the Open, High, Low, Close, and Close_diff time-series.

* Pivot the tickers in the Name column of df_train to the column names of the above DataFrames and set the values as the daily prices

4. Transform each time-series so that it's stationary.

* We do this by detrending with the pd.diff() method

5. Finally, remove the missing data.

#traning dataset

df_train = df.loc['2006-01-03':'2015-01-01']

df_train.tail()

| Open | High | Low | Close | Volume | Name | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2014-12-24 | 50.19 | 50.92 | 50.19 | 50.65 | 5962870 | Altaba |

| 2014-12-26 | 50.65 | 51.06 | 50.61 | 50.86 | 5170048 | Altaba |

| 2014-12-29 | 50.67 | 51.01 | 50.51 | 50.53 | 6624489 | Altaba |

| 2014-12-30 | 50.35 | 51.27 | 50.35 | 51.22 | 10703455 | Altaba |

| 2014-12-31 | 51.54 | 51.68 | 50.46 | 50.51 | 9305013 | Altaba |

#testing dataset

df_validate = df.loc['2015-01-01':'2017-12-31']

df_validate.tail()

| Open | High | Low | Close | Volume | Name | |

|---|---|---|---|---|---|---|

| Date | ||||||

| 2017-12-22 | 71.42 | 71.87 | 71.22 | 71.58 | 10979165 | Altaba |

| 2017-12-26 | 70.94 | 71.39 | 69.63 | 69.86 | 8542802 | Altaba |

| 2017-12-27 | 69.77 | 70.49 | 69.69 | 70.06 | 6345124 | Altaba |

| 2017-12-28 | 70.12 | 70.32 | 69.51 | 69.82 | 7556877 | Altaba |

| 2017-12-29 | 69.79 | 70.13 | 69.43 | 69.85 | 6613070 | Altaba |

It's always a good idea to check we didn't lose any data after the split.

#returns True if no data was lost after the split and False otherwise.

df_train.shape[0] + df_validate.shape[0] == df.shape[0]

True

# sets each column as a stock and every row as a daily closing price

df_validate = df_validate.pivot(columns='Name', values='Close')

df_validate.head()

| Name | 3M | Altaba | Amazon | American Express | Apple | Boeing | Caterpillar | Chevron | Cisco Systems | Coca-Cola | ... | Microsoft | Nike | Pfizer | Procter & Gamble | Travelers | United Technologies | UnitedHealth | Verizon | Walmart | Walt Disney |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2015-01-02 | 164.06 | 50.17 | 308.52 | 93.02 | 109.33 | 129.95 | 91.88 | 112.58 | 27.61 | 42.14 | ... | 46.76 | 47.52 | 31.33 | 90.44 | 105.44 | 115.04 | 100.78 | 46.96 | 85.90 | 93.75 |

| 2015-01-05 | 160.36 | 49.13 | 302.19 | 90.56 | 106.25 | 129.05 | 87.03 | 108.08 | 27.06 | 42.14 | ... | 46.32 | 46.75 | 31.16 | 90.01 | 104.17 | 113.12 | 99.12 | 46.57 | 85.65 | 92.38 |

| 2015-01-06 | 158.65 | 49.21 | 295.29 | 88.63 | 106.26 | 127.53 | 86.47 | 108.03 | 27.05 | 42.46 | ... | 45.65 | 46.48 | 31.42 | 89.60 | 103.24 | 111.52 | 98.92 | 47.04 | 86.31 | 91.89 |

| 2015-01-07 | 159.80 | 48.59 | 298.42 | 90.30 | 107.75 | 129.51 | 87.81 | 107.94 | 27.30 | 42.99 | ... | 46.23 | 47.44 | 31.85 | 90.07 | 105.00 | 112.73 | 99.93 | 46.19 | 88.60 | 92.83 |

| 2015-01-08 | 163.63 | 50.23 | 300.46 | 91.58 | 111.89 | 131.80 | 88.71 | 110.41 | 27.51 | 43.51 | ... | 47.59 | 48.53 | 32.50 | 91.10 | 107.18 | 114.65 | 104.70 | 47.18 | 90.47 | 93.79 |

5 rows × 31 columns

#creates a new column with the difference beteween the closing and opening prices

df_train['Close_Diff'] = df_train.loc[:,'Close'] - df_train.loc[:,'Open']

df_train.head()

| Open | High | Low | Close | Volume | Name | Close_Diff | |

|---|---|---|---|---|---|---|---|

| Date | |||||||

| 2006-01-03 | 77.76 | 79.35 | 77.24 | 79.11 | 3117200 | 3M | 1.35 |

| 2006-01-04 | 79.49 | 79.49 | 78.25 | 78.71 | 2558000 | 3M | -0.78 |

| 2006-01-05 | 78.41 | 78.65 | 77.56 | 77.99 | 2529500 | 3M | -0.42 |

| 2006-01-06 | 78.64 | 78.90 | 77.64 | 78.63 | 2479500 | 3M | -0.01 |

| 2006-01-09 | 78.50 | 79.83 | 78.46 | 79.02 | 1845600 | 3M | 0.52 |

#creates a DataFrame for each time-series (see In [11])

df_train_close = df_train.pivot(columns='Name', values='Close')

df_train_open = df_train.pivot(columns='Name', values='Open')

df_train_close_diff = df_train.pivot(columns='Name', values='Close_Diff')

df_train_high = df_train.pivot(columns='Name', values='High')

df_train_low = df_train.pivot(columns='Name', values='Low')

#makes a copy of the traning dataset

df_train_close_copy = df_train_close.copy()

df_train_close.head()

| Name | 3M | Altaba | Amazon | American Express | Apple | Boeing | Caterpillar | Chevron | Cisco Systems | Coca-Cola | ... | Microsoft | Nike | Pfizer | Procter & Gamble | Travelers | United Technologies | UnitedHealth | Verizon | Walmart | Walt Disney |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2006-01-03 | 79.11 | 40.91 | 47.58 | 52.58 | 10.68 | 70.44 | 57.80 | 59.08 | 17.45 | 20.45 | ... | 26.84 | 10.74 | 23.78 | 58.78 | 45.99 | 56.53 | 61.73 | 30.38 | 46.23 | 24.40 |

| 2006-01-04 | 78.71 | 40.97 | 47.25 | 51.95 | 10.71 | 71.17 | 59.27 | 58.91 | 17.85 | 20.41 | ... | 26.97 | 10.69 | 24.55 | 58.89 | 46.50 | 56.19 | 61.88 | 31.27 | 46.32 | 23.99 |

| 2006-01-05 | 77.99 | 41.53 | 47.65 | 52.50 | 10.63 | 70.33 | 59.27 | 58.19 | 18.35 | 20.51 | ... | 26.99 | 10.76 | 24.58 | 58.70 | 46.95 | 55.98 | 61.69 | 31.63 | 45.69 | 24.41 |

| 2006-01-06 | 78.63 | 43.21 | 47.87 | 52.68 | 10.90 | 69.35 | 60.45 | 59.25 | 18.77 | 20.70 | ... | 26.91 | 10.72 | 24.85 | 58.64 | 47.21 | 56.16 | 62.90 | 31.35 | 45.88 | 24.74 |

| 2006-01-09 | 79.02 | 43.42 | 47.08 | 53.99 | 10.86 | 68.77 | 61.55 | 58.95 | 19.06 | 20.80 | ... | 26.86 | 10.88 | 24.85 | 59.08 | 47.23 | 56.80 | 61.40 | 31.48 | 45.71 | 25.00 |

5 rows × 31 columns

Detrending and Additional Data Cleaning¶

#creates a list of stocks

stocks = df_train_close.columns.tolist()

#list of training DataFrames containing each time-series

df_train_list = [df_train_close, df_train_open, df_train_close_diff, df_train_high, df_train_low]

#detrends each time-series for each DataFrame

for df in df_train_list:

for s in stocks:

df[s] = df[s].diff()

df_train_close.head()

| Name | 3M | Altaba | Amazon | American Express | Apple | Boeing | Caterpillar | Chevron | Cisco Systems | Coca-Cola | ... | Microsoft | Nike | Pfizer | Procter & Gamble | Travelers | United Technologies | UnitedHealth | Verizon | Walmart | Walt Disney |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Date | |||||||||||||||||||||

| 2006-01-03 | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | ... | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN | NaN |

| 2006-01-04 | -0.40 | 0.06 | -0.33 | -0.63 | 0.03 | 0.73 | 1.47 | -0.17 | 0.40 | -0.04 | ... | 0.13 | -0.05 | 0.77 | 0.11 | 0.51 | -0.34 | 0.15 | 0.89 | 0.09 | -0.41 |

| 2006-01-05 | -0.72 | 0.56 | 0.40 | 0.55 | -0.08 | -0.84 | 0.00 | -0.72 | 0.50 | 0.10 | ... | 0.02 | 0.07 | 0.03 | -0.19 | 0.45 | -0.21 | -0.19 | 0.36 | -0.63 | 0.42 |

| 2006-01-06 | 0.64 | 1.68 | 0.22 | 0.18 | 0.27 | -0.98 | 1.18 | 1.06 | 0.42 | 0.19 | ... | -0.08 | -0.04 | 0.27 | -0.06 | 0.26 | 0.18 | 1.21 | -0.28 | 0.19 | 0.33 |

| 2006-01-09 | 0.39 | 0.21 | -0.79 | 1.31 | -0.04 | -0.58 | 1.10 | -0.30 | 0.29 | 0.10 | ... | -0.05 | 0.16 | 0.00 | 0.44 | 0.02 | 0.64 | -1.50 | 0.13 | -0.17 | 0.26 |

5 rows × 31 columns

#counts the missing values in each column

df_train_close.isnull().sum()

Name 3M 1 Altaba 3 Amazon 3 American Express 1 Apple 3 Boeing 1 Caterpillar 1 Chevron 1 Cisco Systems 3 Coca-Cola 1 Exxon Mobil 1 General Electric 1 Goldman Sachs 1 Google 3 Home Depot 1 IBM 1 Intel 3 JPMorgan Chase 1 Johnson & Johnson 1 Mcdonald's 1 Merk 3 Microsoft 3 Nike 1 Pfizer 1 Procter & Gamble 1 Travelers 1 United Technologies 1 UnitedHealth 1 Verizon 1 Walmart 1 Walt Disney 1 dtype: int64

Since the number of missing values in every column is considerably less than 1% of the total number of rows (93,612) we can safely drop them.

#drops all missing values in each DataFrame

for df in df_train_list:

df.dropna(inplace=True)

Building an Asset Correlation Network¶

Now that the data is preprocessed we can start thinking our way through the problem creatively. To refresh our memory, let's restate the problem.

Given the $N$ assets in our portfolio, find a way of computing the allocation weights $w_{i}$, $\Big( \sum_{i=1}^{N}w_{i}=1\Big)$ such that assets more correlated with each other obtain lower weights while those less correlated with each other obtain higher weights.

One way of tackling the above is to think of our portfolio as a weighted graph. Intuitively, a graph captures the relations between objects -- abstract or concrete. Mathematically, a weighted graph is an ordered tuple $G = (V, E, W)$ where $V$ is a set of vertices (or nodes), $E$ is the set of pairwise relationships between the vertices (the edges), and $W$ is a set of numerical values assigned to each edge.

A useful represention of $G$ is the adjacency matrix:

Here the pairwise relations are expressed as the $ij$ entries of an $N \times N$ matrix where $N$ is the number of nodes. In what follows, the adjacency matrix becomes a critical instrument of our asset allocation algorithm. Our strategy is to transform the historical pricing data into a graph with edges weighted by the correlations between each stock. Once the time series data is in this form, we use graph centrality measures and graph algorithms to obtain the desired allocation weights. To construct the weighted graph we adopt the winner-take-all method presented by Tse, et al. (2010) with a few modifications. (See Stock Correlation Network for a summary.) Our workflow in this section is as follows.

- We compute the distance correlation matrix $\rho_{D}(X_{i}, X_{j})$ for the

Open,High,Low,Close, andClose_difftime series. - We use the NetworkX module to transform each distance correlation matrix into a weighted graph.

- We adopt the winner-take-all method and remove edges with correlations below a threshold value of $\rho_{c} = 0.325$,

*Note a threshold value of 0.325 is arbitrary. In practice, the threshold cannot be such that the graph is disconnected, as many centrality measures are undefined for nodes without any connections.

- We inspect the distribution of edges (the so-called degree distribution) for each network. The degree of a node is simply the number of connections it has to other nodes. Algebraically, the degree of the ith vertex is given as,

- Finally, we build a master network by averaging over the edge weights of the

Open,High,Low,Close, andClose_diffnetworks and derive the asset weights from its structure.

What on Earth is Distance Correlation and Why Should We Care?¶

Put simply, Distance correlation is a generalization of Pearson's correlation insofar as it (1) detects both linear and non-linear associations in the data and (2) can be applied to time series of unequal dimension. Below is a comparison of the Distance and Pearson correlation.

Distance correlation varies between 0 and 1. A Distance correlation close to 0 indicates a pair of time series is independent where values close to 1 indicate a high degree of dependence. This is in contrast to Pearson's correlation which varies between -1 and 1 and can be 0 for time series that are dependent (see Szekely, et al. (2017)). What makes Distance correlation particularly appealing is the fact that it can be applied to time series of unequal dimension. If our ultimate goal is to scale the asset allocation algorithm to the entire market (with time series of many assets) and update it in real-time (which it is), the algo must be able to handle time series of arbitrary dimension. The penultimate goal is to observe how an asset correlation network representative of the global market evolves in real-time and update the allocation weights in response.

Calculating the Distance Correlation Matrix with dcor¶

#imports the dcor module to calculate distance correlation

import dcor

#function to compute the distance correlation (dcor) matrix from a DataFrame and output a DataFrame

#of dcor values.

def df_distance_correlation(df_train):

#initializes an empty DataFrame

df_train_dcor = pd.DataFrame(index=stocks, columns=stocks)

#initialzes a counter at zero

k=0

#iterates over the time series of each stock

for i in stocks:

#stores the ith time series as a vector

v_i = df_train.loc[:, i].values

#iterates over the time series of each stock subect to the counter k

for j in stocks[k:]:

#stores the jth time series as a vector

v_j = df_train.loc[:, j].values

#computes the dcor coefficient between the ith and jth vectors

dcor_val = dcor.distance_correlation(v_i, v_j)

#appends the dcor value at every ij entry of the empty DataFrame

df_train_dcor.at[i,j] = dcor_val

#appends the dcor value at every ji entry of the empty DataFrame

df_train_dcor.at[j,i] = dcor_val

#increments counter by 1

k+=1

#returns a DataFrame of dcor values for every pair of stocks

return df_train_dcor

df_train_dcor_list = [df_distance_correlation(df) for df in df_train_list]

df_train_dcor_list[4].head()

| 3M | Altaba | Amazon | American Express | Apple | Boeing | Caterpillar | Chevron | Cisco Systems | Coca-Cola | ... | Microsoft | Nike | Pfizer | Procter & Gamble | Travelers | United Technologies | UnitedHealth | Verizon | Walmart | Walt Disney | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 3M | 1 | 0.353645 | 0.39234 | 0.537989 | 0.349158 | 0.499624 | 0.548548 | 0.504802 | 0.470029 | 0.431732 | ... | 0.455552 | 0.450839 | 0.414834 | 0.401242 | 0.470891 | 0.613992 | 0.359024 | 0.396697 | 0.357485 | 0.535781 |

| Altaba | 0.353645 | 1 | 0.351135 | 0.341589 | 0.290445 | 0.312507 | 0.315713 | 0.267452 | 0.343121 | 0.246817 | ... | 0.302109 | 0.31163 | 0.24649 | 0.218293 | 0.269813 | 0.337054 | 0.211276 | 0.218758 | 0.209349 | 0.37071 |

| Amazon | 0.39234 | 0.351135 | 1 | 0.387674 | 0.373537 | 0.349593 | 0.383719 | 0.31787 | 0.35512 | 0.277101 | ... | 0.340249 | 0.3993 | 0.274551 | 0.220758 | 0.296325 | 0.402777 | 0.244168 | 0.265955 | 0.254739 | 0.402439 |

| American Express | 0.537989 | 0.341589 | 0.387674 | 1 | 0.351312 | 0.468953 | 0.472919 | 0.423415 | 0.455908 | 0.383586 | ... | 0.441841 | 0.450744 | 0.421407 | 0.354739 | 0.476044 | 0.535638 | 0.328788 | 0.393664 | 0.373938 | 0.505921 |

| Apple | 0.349158 | 0.290445 | 0.373537 | 0.351312 | 1 | 0.296182 | 0.388631 | 0.303327 | 0.331026 | 0.235683 | ... | 0.316923 | 0.317469 | 0.224457 | 0.199562 | 0.265335 | 0.343254 | 0.227484 | 0.229273 | 0.191001 | 0.346844 |

5 rows × 31 columns

Building a Time-Series Correlation Network with Networkx¶

#imports the NetworkX module

import networkx as nx

# takes in a pre-processed dataframe and returns a time-series correlation

# network with pairwise distance correlation values as the edges

def build_corr_nx(df_train):

# converts the distance correlation dataframe to a numpy matrix with dtype float

cor_matrix = df_train.values.astype('float')

# Since dcor ranges between 0 and 1, (0 corresponding to independence and 1

# corresponding to dependence), 1 - cor_matrix results in values closer to 0

# indicating a higher degree of dependence where values close to 1 indicate a lower degree of

# dependence. This will result in a network with nodes in close proximity reflecting the similarity

# of their respective time-series and vice versa.

sim_matrix = 1 - cor_matrix

# transforms the similarity matrix into a graph

G = nx.from_numpy_matrix(sim_matrix)

# extracts the indices (i.e., the stock names from the dataframe)

stock_names = df_train.index.values

# relabels the nodes of the network with the stock names

G = nx.relabel_nodes(G, lambda x: stock_names[x])

# assigns the edges of the network weights (i.e., the dcor values)

G.edges(data=True)

# copies G

## we need this to delete edges or othwerwise modify G

H = G.copy()

# iterates over the edges of H (the u-v pairs) and the weights (wt)

for (u, v, wt) in G.edges.data('weight'):

# selects edges with dcor values less than or equal to 0.33

if wt >= 1 - 0.325:

# removes the edges

H.remove_edge(u, v)

# selects self-edges

if u == v:

# removes the self-edges

H.remove_edge(u, v)

# returns the final stock correlation network

return H

#builds the distance correlation networks for the Open, Close, High, Low, and Close_diff time series

H_close = build_corr_nx(df_train_dcor_list[0])

H_open = build_corr_nx(df_train_dcor_list[1])

H_close_diff = build_corr_nx(df_train_dcor_list[2])

H_high = build_corr_nx(df_train_dcor_list[3])

H_low = build_corr_nx(df_train_dcor_list[4])

Plotting a Time-Series Correlation Network with Seaborn¶

import matplotlib.pyplot as plt

import seaborn as sns

%matplotlib inline

# function to display the network from the distance correlation matrix

def plt_corr_nx(H, title):

# creates a set of tuples: the edges of G and their corresponding weights

edges, weights = zip(*nx.get_edge_attributes(H, "weight").items())

# This draws the network with the Kamada-Kawai path-length cost-function.

# Nodes are positioned by treating the network as a physical ball-and-spring system. The locations

# of the nodes are such that the total energy of the system is minimized.

pos = nx.kamada_kawai_layout(H)

with sns.axes_style('whitegrid'):

# figure size and style

plt.figure(figsize=(12, 9))

plt.title(title, size=16)

# computes the degree (number of connections) of each node

deg = H.degree

# list of node names

nodelist = []

# list of node sizes

node_sizes = []

# iterates over deg and appends the node names and degrees

for n, d in deg:

nodelist.append(n)

node_sizes.append(d)

# draw nodes

nx.draw_networkx_nodes(

H,

pos,

node_color="#DA70D6",

nodelist=nodelist,

node_size=np.power(node_sizes, 2.33),

alpha=0.8,

font_weight="bold",

)

# node label styles

nx.draw_networkx_labels(H, pos, font_size=13, font_family="sans-serif", font_weight='bold')

# color map

cmap = sns.cubehelix_palette(3, as_cmap=True, reverse=True)

# draw edges

nx.draw_networkx_edges(

H,

pos,

edge_list=edges,

style="solid",

edge_color=weights,

edge_cmap=cmap,

edge_vmin=min(weights),

edge_vmax=max(weights),

)

# builds a colorbar

sm = plt.cm.ScalarMappable(

cmap=cmap,

norm=plt.Normalize(vmin=min(weights),

vmax=max(weights))

)

sm._A = []

plt.colorbar(sm)

# displays network without axes

plt.axis("off")

#silence warnings

import warnings

warnings.filterwarnings("ignore")

Visualizing How A Portfolio is Correlated with Itself (with Physics)¶

The following visualizations are rendered with the Kamada-Kawai method, which treats each vertex of the graph as a mass and each edge as a spring. The graph is drawn by finding the list of vertex positions that minimize the total energy of the ball-spring system. The method treats the spring lengths as the weights of the graph, which is given by 1 - cor_matrix where cor_matrix is the distance correlation matrix. Nodes seperated by large distances reflect smaller correlations between their time series data, while nodes seperated by small distances reflect larger correlations. The minimum energy configuration consists of vertices with few connections experiencing a repulsive force and vertices with many connections feeling an attractive force. As such, nodes with a larger degree (more correlations) fall towards to the center of the visualization where nodes with a smaller degree (fewer correlations) are pushed outwards. For an overview of physics-based graph visualizations see the Force-directed graph drawing wiki.

# plots the distance correlation network of the daily opening prices from 2006-2014

plt_corr_nx(H_close, title='Distance Correlation Network of the Daily Closing Prices (2006-2014)')

In the above visualization, the sizes of the vertices are proportional to the number of connections they have. The colorbar to the right indicates the degree of disimilarity (the distance) between the stocks. The larger the value (the lighter the color) the less similar the stocks are. Keeping this in mind, several stocks jump out. Apple, Amazon, Altaba, and UnitedHealth all lie on the periphery of the network with the fewest number of correlations above $\rho_{c} = 0.325$. On the other hand 3M, American Express, United Technolgies, and General Electric sit in the core of the network with the greatest number connections above $\rho_{c} = 0.325$. It is clear from the closing prices network that our asset allocation algorithm needs to reward vertices on the periphery and punish those nearing the center. In the next code block we build a function to visualize how the edges of the distance correlation network are distributed.

Degree Histogram¶

# function to visualize the degree distribution

def hist_plot(network, title, bins, xticks):

# extracts the degrees of each vertex and stores them as a list

deg_list = list(dict(network.degree).values())

# sets local style

with plt.style.context('fivethirtyeight'):

# initializes a figure

plt.figure(figsize=(9,6))

# plots a pretty degree histogram with a kernel density estimator

sns.distplot(

deg_list,

kde=True,

bins = bins,

color='darksalmon',

hist_kws={'alpha': 0.7}

);

# turns the grid off

plt.grid(False)

# controls the number and spacing of xticks and yticks

plt.xticks(xticks, size=11)

plt.yticks(size=11)

# removes the figure spines

sns.despine(left=True, right=True, bottom=True, top=True)

# labels the y and x axis

plt.ylabel("Probability", size=15)

plt.xlabel("Number of Connections", size=15)

# sets the title

plt.title(title, size=20);

# draws a vertical line where the mean is

plt.axvline(sum(deg_list)/len(deg_list),

color='darkorchid',

linewidth=3,

linestyle='--',

label='Mean = {:2.0f}'.format(sum(deg_list)/len(deg_list))

)

# turns the legend on

plt.legend(loc=0, fontsize=12)

# plots the degree histogram of the closing prices network

hist_plot(

H_close,

'Degree Histogram of the Closing Prices Network',

bins=9,

xticks=range(13, 30, 2)

)

Observations

- The degree distribution is left-skewed.

- The average node is connected to 86.6% of the network.

- Very few nodes are connected to less than 66.6% of the network.

- The kernel density estimation is not a good fit.

- By eyeballing the plot, the degrees appear to follow an inverse power-law distribution. (This would be consistent with the findings of Tse, et al. (2010)).

plt_corr_nx(

H_close_diff,

title='Distance Correlation Network of the Daily Net Change in Price (2006-2014)'

)

Observations

- The above network has substantially fewer edges than the former.

- Apple, Amazon, Altaba, UnitedHealth, and Merck have the fewest number of correlations above $\rho_{c}$.

- 3M, General Electric, American Express, Walt Disney, and United Technologies have the greatest number of correlations above $\rho_{c}$.

- UnitedHealth is clearly an outlier with only two connections above $\rho_{c}$.

hist_plot(

H_close_diff,

'Degree Histogram of the Daily Net Change in Price Network',

bins=9,

xticks=range(2, 30, 2)

)

Observations:

- The distribution is left-skewed.

- The average node is connected to 73.3% of the network.

- Very few nodes are connected to less than 53.3% of the network.

- The kernel density estimation is a poor fit.

- The degree distribution appears to follow an inverse power-law.

plt_corr_nx(

H_high,

title='Distance Correlation Network of the Daily High Prices (2006-2014)'

)

Observations

- The above network has substantially fewer edges than the former two.

- Apple, Altaba, Amazon, Nike, Mcdonald's, UnitedHealth, Walmart, Procter & Gamble, Verizon, and Merck all lie on the periphery with the fewest number of correlations above $\rho_{c}$.

- UnitedHealth has no correlations above $\rho_{c}$.

- 3M, Walt Disney, General Electric, American Express, United Technologies, and IBM sit in the core with the greatest number of correlations above $\rho_{c}$.

hist_plot(

H_high,

'Degree Histogram of the Daily High Prices Network',

bins=6,

xticks=range(0,25,2)

)

Observations

- In contrast to the Daily Closing and Net Change in Price networks, the Daily High network is not significantly skewed.

- The average node is connected to 53.3% of the network.

- The kernel density estimation most closely resembles a Gaussian.

The degree distribution of the daily high prices certaintly stands out. It is the only distribution that is most resembling a Gaussian --- something you expect to see if the data is truly random. This suggests daily high prices are driven mainly by impulse buys more reflective of random dice rolling than fundamentals.

plt_corr_nx(

H_low,

title='Distance Correlation Network of the Daily Low Prices (2006-2014)'

)

Observations

- The number of edges is comparable to the Daily Closing and Net Change in Price Networks.

- Apple, Amazon, Altaba, UnitedHealth, Walmart, Procter & Gamble, Merck, and Mcdonald's have the fewest number of correlations above $\rho_{c}$.

- 3M, American Express, United Technologies, Walt Disney, JPMorgan Chase, and General Electric have the greatest number of correlations above $\rho_{c}$.

- UnitedHealth has the overall fewest number of correlations above $\rho_{c}$.

hist_plot(

H_low,

'Degree Histogram of the Daily Low Prices Network',

bins=9,

xticks=range(5, 30, 3)

)

Observations

- The degree distribution of the Daily Low Prices network is left skewed.

- The average node is connected to 73.3% of the network.

- Most nodes are connected to greater than 66.6% of the network.

- Few nodes are connected to less than 50% of the network.

- The kernel density estimator is a poor fit.

plt_corr_nx(

H_open,

title='Distance Correlation Network of the Daily Opening Prices (2006-2014)'

)

Observations

- The number of edges of the Daily Opening Prices network is comparable to the the Daily Closing Prices network.

- Apple, Amazon, Altaba, UnitedHealth, Walmart, Verizon, Procter & Gamble, and Merck have the fewest number of correlations above $\rho_{c}$.

- 3M, General Electric, United Technologies, JPMorgan Chase, and American Express have the greatest number of correlations above $\rho_{c}$.

- Unitedhealth has the overall fewest number of correlations above $\rho_{c}$.

hist_plot(

H_open,

'Degree Histogram of the Daily Opening Prices Network',

bins=8,

xticks= range(5, 30, 3)

)

Observations

- The degree distribution is strongly left skewed.

- The average node is connected to 80% of the network.

- Few nodes are connected to less than 50% of the network.

- The kernel density estimation provides a poor fit.

- The degree distribution appears to follow an inverse power-law.

The Hedgecrafted Portfolio¶

# initializes a DataFrame full of zeros

df_zeros = pd.DataFrame(index=stocks, columns=stocks).fillna(0)

# iterates over the length of the DataFrame list containg the Open, High, Low, Close, and Close_diff

# time series

for i in range(len(df_train_list)):

# Adds the distance correlation DataFrames of the Open, High, Low, Close, and Close_diff

# time series together

df_zeros += df_train_dcor_list[i]

# Takes the average of the distance correlation DataFrames

df_master = df_zeros/len(df_train_list)

# Builds the master network with the averaged distance correlation DataFrame

H_master = build_corr_nx(df_master)

# Plots the master network

plt_corr_nx(

H_master,

title='Mean Distance Correlation Network of Historical Stock Prices from (2006-2014)'

)

Observations

- Apple, Amazon, Altaba, UnitedHealth, Walmart, Procter & Gamble, and Merck have the fewest number of correlations above $\rho_{c}$.

- General Electric, American Express, 3M, United Technologies, and Walt Disney have the greatest number of correlations above $\rho_{c}$.

- UnitedHealth is the least correlated stock in our portfolio, followed by Altaba and Apple.

- 3M is the most correlated, followed by United Technologies and American Express.

hist_plot(

H_master,

'Degree Histogram of the Master Network',

bins=9,

xticks=range(3, 30, 3)

)

Observations

- The degree distribution is left skewed.

- The average node is connected to 76.6% of the network.

- Most nodes are connected to 66.6% of the network.

- Few nodes are connected to less than 50% of the network.

Communicability as a Measure of Relative Risk¶

We are now in a position to devise a method to compute the allocation weights of our portfolio. To recall, this is the problem:

Given the $N$ assets in our portfolio, find a way of computing the allocation weights $w_{i}$, $\Big( \sum_{i=1}^{N}w_{i}=1\Big)$ such that assets more correlated with each other obtain lower weights while those less correlated with each other obtain higher weights.

Theres an infinite number of possible solutions to the above problem. The asset correlation network we built contains information on how our portfolio is interrelated (whose connected to who), but it does not tell us how each asset impacts the other or how those impacts travel throughout the network. If, for example, Apple's stock lost 40% of its value wiping out, say, two years of gains, how would this impact the remaining assets in our portfolio? How easily does this kind of behaviour spread and how can we keep our capital isolated from it? We thus seek a measure of "relative risk" that quantifies not only the correlations between assets, but how those correlations mediate perturbations in the portfolio. Our aim, therefore, is twofold: allocate capital inversely proportional to (1) the correlations between assets and (2) proportional to the "impact resistence" of each asset. As luck would have it, there is a centrality measure that does just this! Let us define the relative risk as follows:

where

is the Communicability Betweenness centrality (Estrada, et al. (2009)) of node $r$. Here

is the number of weighted walks involving only node $r$,

is the so-called communicability between nodes $p$ and $q$,

is the adjacency matrix induced by the distance correlation matrix $\text{Cor}_{ij}$, and $\textbf{E}(r)$ is a matrix such that when added to $\textbf{A}$, yields a new graph $G(r) = (V, E')$ with all edges connecting $r \in V$ removed. The constant $C = (n-1)^2 - (n-1)$ normalizes $\omega_{r}$ such that it takes values between 0 and 1. We can better understand what $\omega_{r}$ is counting by re-writing the matrix exponential as a taylor series:

Rasing the adjacency matrix to the power of $k$ counts all walks from $p$ to $q$ of length $k$. The matrix exponential therefore counts all possible ways of moving from $p$ to $q$ weighted by the inverse factorial of $k$. So the denominator of $\omega_{r}$ counts all weighted walks involving every node. Put simply,

So the communicability betweenness centrality is proportional to the number of connections (correlations) a node has and therefore satisifies the first requirement of relative risk. Next, we explore how this measure quantifies the spread of impacts throughout the network, satisfying our second requirement.

The Physics of what Communicability Measures¶

Estrada & Hatano (2007) provided an ingenius argument showing the communicability of a network is identical to the Green's function of a network. That is, it measures how impacts (or more generally thermal fluctuations) travel from one node to another. Their argument works by treating each node as an oscillator and each edge as a spring (which is what we did to generate the visualization of our asset correlation network). Intuitively, we can draw an analogy between the movement of an asset's price and its motion in a ball-spring system. In this analogy, volatility is equivalent to how energetic the oscillator is. Revisiting the hypothetical scenerio of Apple losing 40% of its value: we can visualize this in our mind's eye as an impact to one of the masses---causing it to violently oscillate. How does this motion propagate throughout the rest of the ball-spring system? Which masses absorb the blow and which reflect it? Communicability betweeness centrality answers this question by counting all possible ways the impact can reach node $r$. Higher values indicate the node has a greater susceptiblility to impacts whereas lower values denote just the opposite.

The Bottom Line¶

The communicability of a network quantifies how impacts spread from one node to another. In the context of an asset correlation network, communicability measures how volatility travels node to node. We aim to position our capital such that it's the most resistant to the communicability of volatility. Recall we seek a portfolio that (1) consistently generates wealth while minimizing potential losess and (2) is robust against large market fluctuations and economic downturns. Of course, generous returns are desired, but not in a way that threatens our initial investment. To this end, the strategy moving forward is this: allocate capital inversely proportional to its relative (or intraportfolio) risk.

Intraportfolio Risk¶

# calculates the communicability betweeness centrality and returns a dictionary

risk_alloc = nx.communicability_betweenness_centrality(H_master)

# converts the dictionary of degree centralities to a pandas series

risk_alloc = pd.Series(risk_alloc)

# normalizes the degree centrality

risk_alloc = risk_alloc / risk_alloc.sum()

# resets the index

risk_alloc.reset_index()

# converts series to a sorted DataFrame

risk_alloc = (

pd.DataFrame({"Stocks": risk_alloc.index, "Risk Allocation": risk_alloc.values})

.sort_values(by="Risk Allocation", ascending=True)

.reset_index()

.drop("index", axis=1)

)

with sns.axes_style('whitegrid'):

# initializes figure

plt.figure(figsize=(8,10))

# plots a pretty seaborn barplot

sns.barplot(x='Risk Allocation', y='Stocks', data=risk_alloc, palette="rocket")

# removes spines

sns.despine(right=True, top=True, bottom=True)

# turns xticks off

plt.xticks([])

# labels the x axis

plt.xlabel("Relative Risk %", size=12)

# labels the y axis

plt.ylabel("Historical Portfolio (2006-2014)", size=12)

# figure title

plt.title("Intraportfolio Risk", size=18)

# iterates over the stocks (label) and their numerical index (i)

for i, label in enumerate(list(risk_alloc.index)):

# gets the height of each bar in the barplot

height = risk_alloc.loc[label, 'Risk Allocation']

# gets the relative risk as a percentage (the labels)

label = (risk_alloc.loc[label, 'Risk Allocation']*100

).round(2).astype(str) + '%'

# annotates the barplot with the relative risk percentages

plt.annotate(str(label), (height + 0.001, i + 0.15))

We read an intraportfolio risk plot like this: Altaba is $\dfrac{0.47}{0.09} = 4.66$ times riskier than UnitedHealth (UNH), Apple is $\dfrac{1.01}{0.09} = 11.22$ times more risky than UNH, ... , and 3M is a whopping $\dfrac{4.17}{0.09} = 46.33$ times riskier than UNH! Conversely, 3M is $\dfrac{4.17}{4.11} = 1.01$ times as risky as United Technologies, $\dfrac{4.17}{4.11} = 1.01$ times as risky as American Express, so on and so forth. Intuitively, the assets that cluster in the center of the network are most susceptible to impacts, whereas those further from the cluster are the least susceptible. The logic from here is straightforward: take the inverse of the relative risk (which we call the "relative certainty") and normalize it such that it adds to 1. These are the asset weights. Formally,

Next, Let's visualize the allocation of 10,000 (USD) in our portfolio.

Communicability-Based Asset Allocation¶

# calculates degree centrality and assigns it to investmnet_A

investment_A = nx.communicability_betweenness_centrality(H_master)

# calculates the inverse of the above and re-asigns it to investment_A as a pandas series

investment_A = 1 / pd.Series(investment_A)

# normalizes the above

investment_A = investment_A / investment_A.sum()

# resets the index

investment_A.reset_index()

# converts the above series to a sorted DataFrame

investment_A = (

pd.DataFrame({"Stocks": investment_A.index, "Asset Allocation": investment_A.values})

.sort_values(by="Asset Allocation", ascending=False)

.reset_index()

.drop("index", axis=1)

)

with sns.axes_style('whitegrid'):

# initializes a figure

plt.figure(figsize=(8,9))

# plot a pretty seaborn barplot

sns.barplot(x='Asset Allocation', y='Stocks', data=investment_A, palette="Greens_r")

# despines the figure

sns.despine(right=True, top=True, bottom=True)

# turns xticks off

plt.xticks([])

# turns the x axis label off

plt.xlabel('')

# fig title

plt.title("Asset Allocation: 10,000 (USD)", size=12)

# y axis label

plt.ylabel("Historical Hedgecrafted Portfolio", size=12)

# captial to be allocated

capital = 10000

# iterates over the stocks (label) and their numerical indices (i)

for i, label in enumerate(list(investment_A.index)):

# gets the height of each bar

height = investment_A.loc[label, 'Asset Allocation']

# calculates the capital to be allocated

label = (investment_A.loc[label, 'Asset Allocation'] * capital

).round(2)

# annotes the capital above each bar

plt.annotate('${:,.0f}'.format(label), (height + 0.002, i + 0.15))

UnitedHealth recieves nearly 50%, Altaba gets about 10%, Apple 4%, Merck 2%, and the remaining assets recieve less than 2% of our capital. To the traditional invester, this strategy may appear "risky" since 60% of our investment is with 2 of our 31 assets. While it's true if UnitedHealth is hit hard we'll lose a substantial amount of money, our algorithm predicts UnitedHealth is the least likey to take a hit if and when our other assets get in trouble. UnitedHealth is clearly the winning pick in our portfolio.

It's worth pointing out that the methods we've used to generate the asset allocation weights differ dramatically from the contemporary methods of MPT and its extensions. The approach taken in this project makes no assumptions of future outcomes of a portfolio, i.e., the algorithm doesn't require us to make a prediction of the expected returns (as MPT does). What's more---we're not solving an optimization problem---there's nothing to be minimized or maximized. Instead, we observe the topology (interrelatedness) of our portfolio, predict which assets are the most susceptible to the communicability of volatile behaviour and allocate capital accordingly.

# DataFrame of the prices we buy stock at

df_buy_in = df_train_close_copy.loc['2014-12-31'].sort_index().to_frame('Buy In: 2014-12-31')

Alternative Allocation Strategy: Allocate Capital in the Maximum Independent Set¶

The maximum independent set (MIS) is the largest set of vertices such that no two are adjacent. Applied to our asset correlation network, the MIS is the greatest number of assets such that every pair has a correlation below $\rho_{c} = 0.325$. The size of the MIS is inversely proportional to the threshold $\rho_{c}$. Larger values of $\rho_{c}$ produce a sparse network (more edges are removed) and therefore the MIS tends to be larger. An optimized portfolio would therefore correspond to maximizing the size of the MIS subject to minimizing $\rho_{c}$. The best way to do this is to increase the universe of assets we're willing to invest in. By further diversifying the portfolio with many asset types and classes, we can isolate the largest number of minimally correlated assets and allocate capital inversely proportional to their relative risk. While generating the asset weights remains a non-optimization problem, generating the asset correlation network becomes one. We're really solving two sepreate problems: determing how to build the asset correlation network (there are many) and determining which graph invariants (there are many) extract the asset weights from the network. As such, one can easily imagine a vast landscape of portfolios beyond that of MPT and a metric fuck-tonne of wealth to create. Unfortunately, solving the MIS problem is NP-hard. The best we can do is find an approximation.

Using Expert Knowledge to Approximate the Maximum Independent Set¶

We have two options: randomly generate a list of maximal indpendent sets (subgraphs of $G$ such that no two vertices share an edge) and select the largest one, or use expert knowledge to reduce the number of sets to generate and do the latter. Both methods are imperfect, but the former is far more computationally expensive than the latter. Suppose we do fundamentals research and conclude UnitedHealth and Amazon must be in our portfolio. How could we imbue the algorithm with this knowledge? Can we make the algorithm flexible enough for portfolio managers to fine-tune with goold-ole' fashioned research, while at the same time keeping it rigged enough to prevent poor decisions from producing terribe portfolios? We confront this problem in the code block below by extracting an approximate MIS by generating 100 random maximal indpendent sets containing UnitedHealth and Amazon.

# a function to generate a random approximate MIS

### WARNING: rerunning kernel will produce different MISs

def generate_mis(G, sample_size, nodes=None):

"""Returns a random approximate maximum independent set.

Parameters

----------

G: NetworkX graph

Undirected graph

nodes: list, optional

a list of nodes the approximate maximum independent set must contain.

sample_size: int

number of maximal independent sets sampled from

Returns

-------

max_ind_set: list or None

list of nodes in the apx-maximum independent set

NoneType object if any two specified nodes share an edge

"""

# list of maximal independent sets

max_ind_set_list=[]

# iterates from 0 to the number of samples chosen

for i in range(sample_size):

# for each iteration generates a random maximal independent set that contains

# UnitedHealth and Amazon

max_ind_set = nx.maximal_independent_set(G, nodes=nodes, seed=i)

# if set is not a duplicate

if max_ind_set not in max_ind_set_list:

# appends set to the above list

max_ind_set_list.append(max_ind_set)

# otherwise pass duplicate set

else:

pass

# list of the lengths of the maximal independent sets

mis_len_list=[]

# iterates over the above list

for i in max_ind_set_list:

# appends the lengths of each set to the above list

mis_len_list.append(len(i))

# extracts the largest maximal independent set, i.e., the maximum independent set (MIS)

## Note: this MIS may not be unique as it is possible there are many MISs of the same length

max_ind_set = max_ind_set_list[mis_len_list.index(max(mis_len_list))]

return max_ind_set

max_ind_set = generate_mis(H_master, nodes=['UnitedHealth', 'Amazon', 'Verizon'], sample_size=100)

print(max_ind_set)

['Amazon', 'UnitedHealth', 'Verizon', "Mcdonald's"]

The generate_mis function generates a maximal independent set that approximates the true maximum independent set. As an option, the user can pick a list of assets they want in their portfolio and generate_mis will return the safest assets to complement the user's choice. Picking UNH and AMZN left us with VZ and MCD. The weights of these assets will remain directly inversely proportional to the communicability betweeness centrality.

# prices of shares to buy for the MIS

df_mis_buy_in = df_buy_in.loc[list(max_ind_set)]

df_mis_buy_in

| Buy In: 2014-12-31 | |

|---|---|

| Name | |

| Amazon | 310.35 |

| UnitedHealth | 101.09 |

| Verizon | 46.78 |

| Mcdonald's | 93.70 |

Backtesting with Modern Portfolio Theory¶

Now that we have a viable alternative to portfolio optimization, it's time to see how the Hedgecraft portfolio performed in the validation years (15', 16', and 17') with respect to the Markowitz portfolio (i.e., the efficient frontier model) and the overall market. To summarize our workflow thus far we:

- Preprocessed historical pricing data of 31 stocks for time series analyses.

- Computed the distance correlation matrix $\rho_{D}(X_{i}, X_{j})$ for the

Open,High,Low,Close, andClose_difffrom 2006-2014. - Used the NetworkX module to transform each distance correlation matrix into a weighted graph.

- Adopted the winner-take-all method by Tse, et al. and removed edges with correlations below a threshold value of $\rho_{c} = 0.325$.

- Built a master network by averaging over the edge weights of the

Open,High,Low,Close, andClose_diffnetworks. - Calculated the "relative risk" of each asset as the communicabality betweeness centrality assigned to each node.

- Generated the asset weights as the normalized inverse of communicability betweeness centrality.

In addition to the above steps, we introduced a human-in-the-middle strategy, giving the user flexible control over the portfolio construction process. This is the extra step we added:

- Adjust the asset weights for an approximate maximum independent set, either with or without human intervention.

To distinguish bewteen these two approaches we designate steps 1-7 as the Hedgecraft algo and steps 1-8 as the Hedgecraft MIS algo. Below we observe how these models perform with the Efficient Frontier as a benchmark.

Generating Hedgecraft Portfolio Weights¶

# calculates communicability betweeness centrality

weights = nx.communicability_betweenness_centrality(H_master)

# dictionary comprehension of communicability centrality for the maximum independent set

mis_weights = {key: weights[key] for key in list(max_ind_set)}

# a function to convert centrality scores to portfolio weights

def centrality_to_portfolio_weights(weights):

"""Returns a dictionary of portfolio weights.

Parameters

----------

weights: dictionary

NetworkX centrality scores

Returns

-------

portfolio weights: dictionary

normalized inverse of chosen centrality measure

"""

# iterates over the key, value pairs in the weights dict

for key, value in weights.items():

# takes the inverse of the communicability betweeness centrality of each asset

weights[key] = 1/value

# normalization parameter for all weights to add to 1

norm = 1.0 / sum(weights.values())

# iterates over the keys (stocks) in the weights dict

for key in weights:

# updates each key value to the normalized value and rounds to 3 decimal places

weights[key] = round(weights[key] * norm, 3)

return weights

print(centrality_to_portfolio_weights(weights))

print('\n')

print(centrality_to_portfolio_weights(mis_weights))

{'3M': 0.011, 'Altaba': 0.105, 'Amazon': 0.019, 'American Express': 0.011, 'Apple': 0.044, 'Boeing': 0.014, 'Caterpillar': 0.012, 'Chevron': 0.012, 'Cisco Systems': 0.011, 'Coca-Cola': 0.013, 'Exxon Mobil': 0.012, 'General Electric': 0.011, 'Goldman Sachs': 0.013, 'Google': 0.014, 'Home Depot': 0.012, 'IBM': 0.011, 'Intel': 0.011, 'JPMorgan Chase': 0.011, 'Johnson & Johnson': 0.011, "Mcdonald's": 0.013, 'Merk': 0.02, 'Microsoft': 0.012, 'Nike': 0.013, 'Pfizer': 0.013, 'Procter & Gamble': 0.016, 'Travelers': 0.012, 'United Technologies': 0.011, 'UnitedHealth': 0.49, 'Verizon': 0.014, 'Walmart': 0.019, 'Walt Disney': 0.011}

{'Amazon': 0.035, 'UnitedHealth': 0.914, 'Verizon': 0.026, "Mcdonald's": 0.025}

Hedgecraft MIS allocates a staggering 91.4% of the investment to UNH. At first sight this portfolio appears far less diversified than Hedgecraft. However, if we recall, the relative risk of UNH was two orders of magnitude smaller than every other security (with the sole exception of Altaba). If our only options are the above 31 securities, the algorithm predicts UNH is the safest pick and allocates accordingly.

Allocating Shares to the Hedgecraft Portfolio¶

# imports a tool to convert capital into shares

from pypfopt import discrete_allocation

# returns the number of shares to buy given the asset weights, prices, and capital to invest

alloc = discrete_allocation.DiscreteAllocation(

weights,

df_buy_in['Buy In: 2014-12-31'],

total_portfolio_value=capital

)

# returns same as above but for the MIS

mis_alloc = discrete_allocation.DiscreteAllocation(

mis_weights,

df_mis_buy_in['Buy In: 2014-12-31'],

total_portfolio_value=capital

)

0 out of 31 tickers were removed 0 out of 4 tickers were removed

alloc = alloc.greedy_portfolio()[0]

mis_alloc = mis_alloc.greedy_portfolio()[0]

# converts above shares to a pandas series

alloc_series = pd.Series(alloc, name='Shares')

# names the series

alloc_series.index.name = 'Assets'

# resets index, prints assets with the shares we buy

alloc_series.reset_index

print(alloc_series)

print('\n')

# does same as above but for the MIS

mis_alloc_series = pd.Series(mis_alloc, name='MIS Shares')

mis_alloc_series.index.name = 'Assets'

mis_alloc_series.reset_index

print(mis_alloc_series)

Assets UnitedHealth 48 Altaba 20 Apple 3 Merk 3 Amazon 1 Walmart 2 Procter & Gamble 2 Boeing 1 Google 1 Verizon 2 Coca-Cola 3 Goldman Sachs 1 Mcdonald's 1 Nike 2 Pfizer 4 Caterpillar 1 Chevron 1 Exxon Mobil 1 Home Depot 1 Microsoft 2 Travelers 1 3M 1 American Express 1 Cisco Systems 3 General Electric 4 IBM 1 Intel 3 JPMorgan Chase 1 Johnson & Johnson 1 United Technologies 0 Walt Disney 1 Name: Shares, dtype: int64 Assets UnitedHealth 90 Amazon 1 Verizon 6 Mcdonald's 3 Name: MIS Shares, dtype: int64

# converts Hedgecraft shares series to a DataFrame

df_alloc = alloc_series.sort_index().to_frame('Shares')

# converts Hedgecraft MIS shares series to a DataFrame

df_mis_alloc = mis_alloc_series.sort_index().to_frame('MIS Shares')

The Efficient Frontier¶

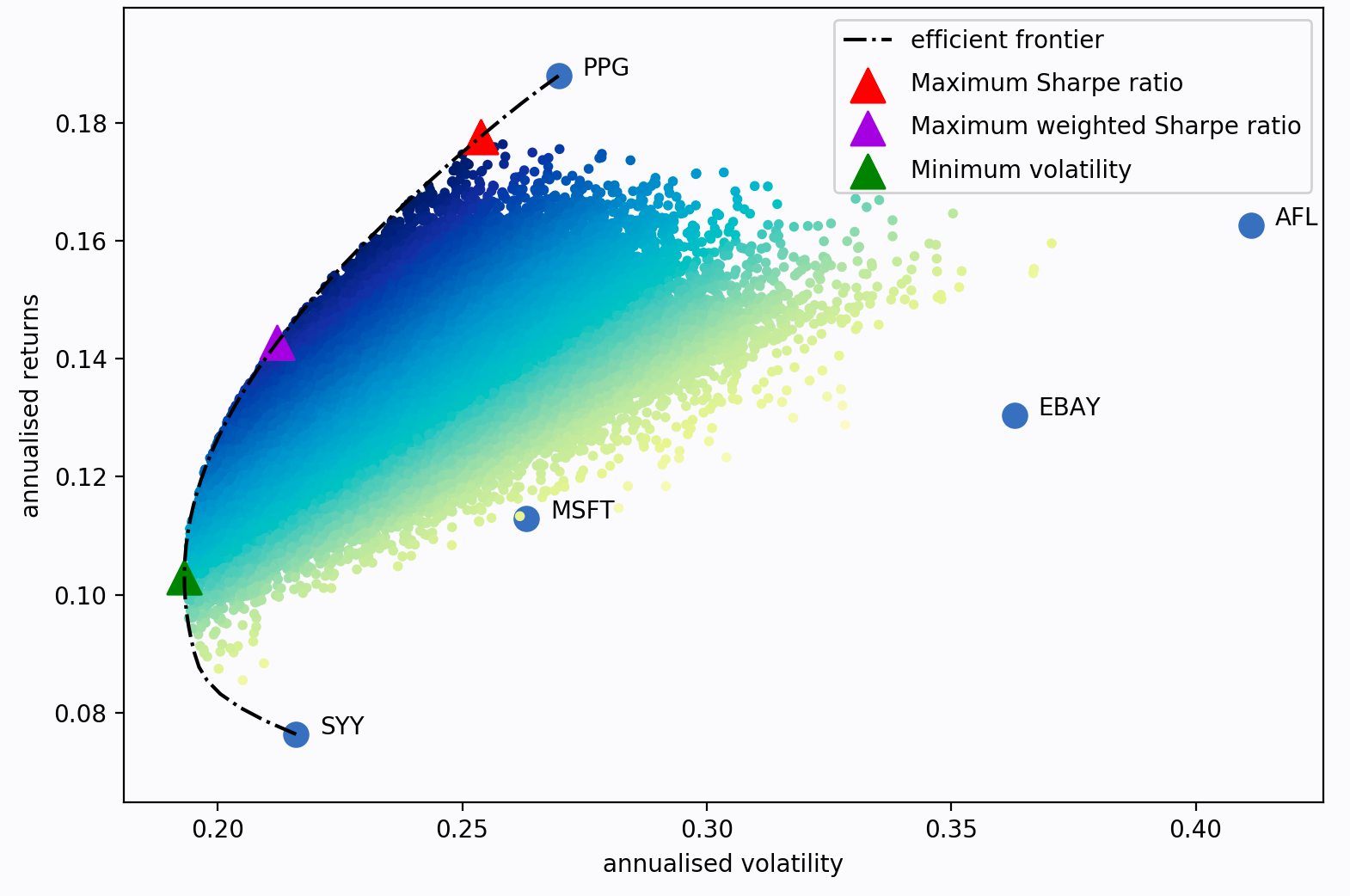

Harry Markowitz's 1952 paper Portfolio Selection transformed portfolio management from an art to a science. Markowitz's key insight came from diversification: by combinining uncorrelated assets with different expected returns and volatilities, one can calculate an optimal allocation.

The main idea is this: if $w$ is the fraction of capital to be allocated to some asset, then the portfolio risk in terms of the covariance matrix $\Sigma$ is given by $w^{\top}\Sigma w$ and its expected returns are given by $w^{\top}\mu$. The optimal portfolio can therefore be regarded as a convex optimization problem, and a solution can be found with quadratic programming. Denoting the target returns as $\mu*$ the optimization problem is mathmeatically expressed as follows:

Varying the target return yields a different set of weights (i.e., a different portfolio). The set of all the portfolios with optimal weights is referred to as the efficient frontier.

Each dot in the above plot represents a different possible portoflio, with darker blue corresponding to better portfolios (in terms of the Sharpe ratio). The dotted black line is the frontier. The triangular markers denote the optimal portfolios subjected to different optimization objectives.

In the code blocks bellow we use the PyPortfolioOpt library to implement the Efficient Frontier algorithm. Rather than optimizing for a maximum Sharpe ratio, we optimize for a minimum volatility as these portfolios tend to outperform portfolio's with a maximized Sharpe ratio.

# imports a tool to calculate the mean historical return from a

# portfolio optimization package called pypfopt

from pypfopt.expected_returns import mean_historical_return

# returns the mean historical return of the training data

mu = mean_historical_return(df_train_close_copy)

# computes the covariance matrix

S = df_train_close_copy.cov()

# imports the efficient frontier model for asset allocation

from pypfopt.efficient_frontier import EfficientFrontier

# runs the efficient frontier (EF) algo

ef = EfficientFrontier(mu, S)

# computes portfolio weights subject to minimizing the volatility (portfolio std)

weights_ef = ef.min_volatility()

# rounds and prints the weights

cleaned_weights = ef.clean_weights()

print(cleaned_weights)

{'3M': 0.0, 'Altaba': 0.0, 'Amazon': 0.0, 'American Express': 0.0, 'Apple': 0.0, 'Boeing': 0.0, 'Caterpillar': 0.0, 'Chevron': 0.0, 'Cisco Systems': 0.62264, 'Coca-Cola': 0.13036, 'Exxon Mobil': 0.0, 'General Electric': 0.0, 'Goldman Sachs': 0.0, 'Google': 0.0, 'Home Depot': 0.0, 'IBM': 0.0, 'Intel': 0.17268, 'JPMorgan Chase': 0.0, 'Johnson & Johnson': 0.0, "Mcdonald's": 0.0, 'Merk': 0.0, 'Microsoft': 0.0, 'Nike': 0.0, 'Pfizer': 0.07431, 'Procter & Gamble': 0.0, 'Travelers': 0.0, 'United Technologies': 0.0, 'UnitedHealth': 0.0, 'Verizon': 0.0, 'Walmart': 0.0, 'Walt Disney': 0.0}

Allocating Shares to the Markowitz Portfolio¶

# returns the number of shares to buy given asset prices, weights, and capital to invest for the EF model

ef_alloc = discrete_allocation.DiscreteAllocation(

weights_ef,

df_buy_in['Buy In: 2014-12-31'],

total_portfolio_value=capital

)

27 out of 31 tickers were removed

ef_alloc = ef_alloc.greedy_portfolio()[0]

# converts EF shares to a pandas series

ef_alloc_series = pd.Series(ef_alloc, name='Shares')

# names the series

ef_alloc_series.index.name = 'Assets'

# resets index, prints assets and the shares we buy

ef_alloc_series.reset_index

<bound method Series.reset_index of Assets Cisco Systems 224 Intel 47 Coca-Cola 31 Pfizer 24 Name: Shares, dtype: int64>

The Efficient Frontier produces a radically different portfolio than Hedgecraft or its MIS variant.

# converts EF shares series to a DataFrame

df_ef_alloc = ef_alloc_series.sort_index().to_frame('Shares')

Portfolio Performance: Hedgecraft vs. Efficient Frontier¶

In this section we write production (almost) ready code for portfolio analysis and include our own risk-adjusted returns score. The section looks something like this:

- We obtain the cumulative returns and returns on investment,

- extract the end of year returns and annual return rates,

- calculate the average annual rate of returns and annualized portfolio standard deviation,

- compute the Sharpe Ratio,

- Maximum Drawdown,

- Returns over Maximum Drawdown,

- and our own unique measure: the Growth-Risk Ratio.

Finally, we visualize the returns, drawdowns, and returns distribution of each model and analyze the results.

# total capital invested in the Hedgecraft portfolio after buying shares

capital = (df_buy_in['Buy In: 2014-12-31']*df_alloc['Shares']).sum()

# total capital invested in Efficient Frontier portfolio after buying shares

ef_capital = (df_buy_in['Buy In: 2014-12-31']*df_ef_alloc['Shares']).sum()

# total capital invested in Hedgecraft MIS portfolio after buying shares

mis_capital = (df_mis_buy_in['Buy In: 2014-12-31']*df_mis_alloc['MIS Shares']).sum()

# function to compute the cumulative returns of a portfolio

def cumulative_returns(shares_allocation, capital, test_data):

"""Returns the cumulative returns of a portfolio.

Parameters

----------

shares_allocation: DataFrame

number of shares allocated to each asset in the portfolio

capital: float

total amount of money invested in the portfolio

test_data: DataFrame

daily closing prices of portfolio assets

Returns

-------

cumulative_daily_returns: Series

cumulative daily returns of the portfolio

"""

# list of DataFrames of cumulative returns for each stock

daily_returns = []

# iterates over every stock in the portfolio

for stock in shares_allocation.index:

# multiples shares by share prices in the validation dataset

daily_returns.append(shares_allocation.loc[stock].values * test_data[stock])

# concatenates every DataFrame in the above list to a single DataFrame

daily_returns_df = pd.concat(daily_returns, axis=1).reset_index()

# sets the index as the date

daily_returns_df.set_index("Date", inplace=True)

# adds the cumulative returns for every stock

cumulative_daily_returns = daily_returns_df.sum(axis=1)

# returns the cumulative daily returns of the portfolio

return cumulative_daily_returns

# Hedgecraft cumulative daily returns

total_daily_returns = cumulative_returns(

df_alloc,

capital,

df_validate

).rename('Hedgecraft Cumulative Daily Returns')

# Efficient Frontier cumulative daily returns

ef_total_daily_returns = cumulative_returns(

df_ef_alloc,

ef_capital,

df_validate

).rename('EF Cumulative Daily Returns')

# Hedgecraft MIS cumulative daily returns

mis_total_daily_returns = cumulative_returns(

df_mis_alloc,

mis_capital,

df_validate

).rename('MIS Cumulative Daily Returns')

# function to compute daily return on investment (roi)

def portfolio_daily_roi(shares_allocation, capital, test_data):

"""Returns the daily return on investment.

Parameters

----------

shares_allocation: DataFrame

number of shares allocated to each asset

capital: float

total amount of money invested in the portfolio

test_data: DataFrame

daily closing prices of each asset

Returns

-------

daily_roi: Series

daily return on investment of the portfolio

"""

# computes the cumulative returns

cumulative_daily_returns = cumulative_returns(

shares_allocation,

capital,

test_data

)

# calculates daily return on investment

daily_roi = cumulative_daily_returns.apply(

lambda returns: ((returns - capital) / capital)*100

)

# returns the daily return on investment

return daily_roi

# Hedgecraft daily return on investment

daily_roi = portfolio_daily_roi(

df_alloc,

capital,

df_validate

).rename('Hedgecraft Daily Returns')

# Efficient Frontier daily return on investment

ef_daily_roi = portfolio_daily_roi(

df_ef_alloc,

ef_capital,

df_validate

).rename('EF Daily Returns')

# Hedgecraft MIS daily return on investment

mis_daily_roi = portfolio_daily_roi(

df_mis_alloc,

mis_capital,

df_validate

).rename('MIS Daily Returns')

End of Year Returns¶

# imports datetime manipluation library

from datetime import datetime

# function to extract the end of year returns

def end_of_year_returns(model_roi, return_type, start, end):

"""Returns the end of year returns of a portfolio.

Parameters

----------

model_roi: Series

portoflio returns on investment

return_type: string

'returns': returns roi

'returns_rate': returns rate of returns

start: int

starting year to extract last trading day from

end: int

ending year to extract last trading day from

Returns

-------

end_of_year_returns: dictionary

each year's returns or rate of returns

"""

# converts index of datetimes to a list of strings

dates = model_roi.index.astype('str').tolist()

# list comprehension of a string of dates between the

# start and end dates

years = [str(x) for x in range(start, end + 1)]

# generates an empty list of lists for each year

end_year_dates = [[] for _ in range(len(years))]

# iterates over every date in the roi series

for date in dates:

# iterates over every year in the years list

for year in years:

# iterates over every year in each date

if year in date:

# converts each date string to a datime object

datetime_object = datetime.strptime(date, '%Y-%m-%d')

# appends each date to its corresponding year in the years list

(end_year_dates[years.index(year)]

.append(datetime.strftime(datetime_object, '%Y-%m-%d')))

# finds the last date in each year

end_year_dates = [max(x) for x in end_year_dates]

# gets the rounded end of year returns

returns = [round(model_roi[date], 1) for date in end_year_dates]

# shifts the returns list by 1 and appends 0 to the beginning of the list

return_rates = [0] + returns[:len(returns)-1]

"""Example: [a, b, c] -> [0, a, b]"""

# converts returns list to an array

returns_arr = np.array(returns)

# converts the return_rates list to an array

return_rates_arr = np.array(return_rates)

# calculates the rounded rate of returns

return_rates = [round(x, 1) for x in list(returns_arr - return_rates_arr)]

"""Example: [a, b, c] - [0, a, b] = [a, b-a, c-b]"""

# dictionary with the years as keys and returns as values

returns = dict(zip(years, returns))

# dictionary with the years as keys and return rates as values

return_rates = dict(zip(years, return_rates))

if return_type == 'returns':

return returns

if return_type == 'return_rates':

return return_rates

# Hedgecraft annual return rates

returns_dict = end_of_year_returns(

daily_roi,

'return_rates',

2015,

2017

)

# Efficient Frontier annual return rates

ef_returns_dict = end_of_year_returns(

ef_daily_roi,

'return_rates',

2015,

2017

)

# Hedgecraft MIS annual return rates

mis_returns_dict = end_of_year_returns(

mis_daily_roi,

'return_rates',

2015,

2017

)

# Hedgecraft annual returns

tot_returns_dict = end_of_year_returns(

daily_roi,

'returns',

2015,

2017

)

# Efficient Frontier annual returns

ef_tot_returns_dict = end_of_year_returns(

ef_daily_roi,

'returns',

2015,

2017

)

# Hedgecraft MIS annual returns

mis_tot_returns_dict = end_of_year_returns(

mis_daily_roi,

'returns',

2015,

2017

)

Average Annual Rate of Returns¶

# function to calculate avg annual portfolio returns

def avg_annual_returns(end_of_year_returns, mstat):

"""Returns average annual returns.

Parameters

----------

end_of_year_returns: dictionary

annual returns

mstat: string

'arithmetic': returns the arithmetic mean

'geometric': returns the geometric mean

Returns

-------

average annual returns: float

"""

# imports mean stats

from scipy.stats import mstats

# converts returns dict to an array (in decimal fmt)

returns_arr = np.array(list(end_of_year_returns.values()))/100

if mstat == 'geometric':

# calculates the geometric mean

gmean_returns = (mstats.gmean(1 + returns_arr) - 1)*100

return round(gmean_returns, 2)

if mstat == 'arithmetic':

# calculates the arithmetic mean

mean_returns = np.mean(returns_arr)

return round(mean_returns, 2)

# Hedgecraft avg annual returns

gmean_returns = avg_annual_returns(returns_dict, mstat='geometric')

# Efficient Frontier avg annual returns

ef_gmean_returns = avg_annual_returns(ef_returns_dict, mstat='geometric')

# Hedgecraft MIS avg annual returns

mis_gmean_returns = avg_annual_returns(mis_returns_dict, mstat='geometric')

print(gmean_returns)

print(ef_gmean_returns)

print(mis_gmean_returns)

27.42 9.62 38.7

Annualized Portfolio Standard Deviation¶

The annualized standard deviation (a.k.a volatility) measures how far the portfolio's returns vary from the mean, that is, it measures how spread out the data is. It can be readily calculated as:

where $252$ is the number of trading days in a year, $\textbf{w}$ is the vector of portfolio weights, and $\mathbf{\Sigma}$ is the covariance matrix.

# function to calculate annualized portoflio standard deviation

def portfolio_std(weights, test_data):

"""Returns annualized portfolio volatility.

Parameters

----------

weights: dictionary

portfolio weights

test_data: DataFrame

validation data set

Returns

-------

portfolio_std_dev: float

annualized portfolio standard deviaion

"""

# computes daily change in returns from 2015-2017

daily_ret_delta = test_data.pct_change()

# computes the covariance matrix of the above

cov_matrix = daily_ret_delta.cov()

# initializes weights

weights_list = []

# iterates over weights dict and appends above list

for key, value in weights.items():

weights_list.append(value)

# converts weights list to numpy array

weights_arr = np.array(weights_list)

# calculates the annualized portfolio standard deviation from 2015-2017 in pct format

portfolio_std_dev = np.sqrt(

np.dot(

weights_arr.T,

np.dot(

cov_matrix,

weights_arr

)

)

)*np.sqrt(252)*100

return round(portfolio_std_dev, 2)

# function to calculate annualized portfolio standard deviation with a

# maximum independent set parameter

def mis_portfolio_std(weights, test_data, maximum_independent_set):

"""Returns annualized portfolio volatility.

Parameters

----------

weights: dictionary

portfolio weights

test_data: DataFrame

validation data set

maximum_independent_set: list

largest list of assets such that no two are adjacent

Returns

-------

portfolio_std_dev: float

annualized portfolio standard deviation

"""

# computes daily change in returns from 2015-2017

daily_ret_delta = test_data[maximum_independent_set].pct_change()

# computes the covariance matrix

cov_matrix = daily_ret_delta.cov()

# initializes weights list

weights_list = []

# iterates over weights dict and appends above list

for key, value in weights.items():

weights_list.append(value)

# converts weights list to numpy array

weights_arr = np.array(weights_list)

# calculates portfolio standard deviation from 2015-2017