Chapter 3 - Linear Regression¶

ISLR 3장의 Linear Regression Python 실습¶

Linear Regression (선형 회귀분석)##¶

- Response의 값이 숫자인 labeled 데이타를 이용하는 Regression 타입 Supervised Learning 모델

- 빨리 돌고, 오랜 시간 많이 연구되어 특성을 잘 알고, 모델의 해석이 쉬워 널리 사용

사용할 주요 Python 패키지¶

- pandas : 데이터 입출력, Munging, & etc.

- numpy : 수식 계산

- matplotlib : 시각화

- seaborn : 시각화

- statsmodels : 통계모델

- scikit-learn : 머신러닝

* Statsmodels 패키지의 모델을 사용해 Linear Regression을 익힌다.*¶

Statsmodels 의 Linear Regression 모델은 ISLR 책의 R 쓰임새와 비슷하게 사용할 수 있음

# 패키지 imports

import pandas as pd

import numpy as np

import matplotlib.pyplot as plt

import seaborn

import statsmodels.formula.api as smf # R의 formula 식 유사하게 쓰임

from hblee import st,Corrplot # hblee.py: 웹에서 훔쳤거나, 생각없이 짠 단순 맹한 클래스 & 함수

# notebook에 직접 그래프를 plot

%matplotlib inline

import sys

print(sys.executable)

print(sys.version)

print(sys.version_info)

/home/lee/Programs/anaconda3/bin/python 3.6.0 |Anaconda custom (64-bit)| (default, Dec 23 2016, 12:22:00) [GCC 4.4.7 20120313 (Red Hat 4.4.7-1)] sys.version_info(major=3, minor=6, micro=0, releaselevel='final', serial=0)

실행 환경¶

- Python 3.6.0

- Anaconda 4.3.0

- 추가로 seaborn : "conda install seaborn"

- 추가로 colormap & easydev : "pip install colormap easydev"

np.__version__ , pd.__version__, seaborn.__version__

('1.11.3', '0.19.2', '0.8.0')

# package_list = ['pandas', 'numpy', 'IPython', 'seaborn', 'sklearn', 'matplotlib', 'statsmodels']

# for pack in package_list:

# statement = 'import ' + pack

# exec(statement)

# print ("%s : %s" % (pack, eval(pack).__version__) )

Data Load¶

- 책에서 사용한 Advertising 데이터를 load 함.

- local 머신에서 로딩할 수도, 또는 웹에서 직접 갖고 올 수도 있다. 로딩하기 전에 데이터 구조를 잘 살핍시다

# 웹에서 직접 pandas의 DataFrame으로 읽음. 첫째 column을 row index로 사용.

# 아래의 웹에서 가져 온 csv 파일의 column명이 소문자로 시작하여 에러를 일으킴. 주의...

# advertising = pd.read_csv('http://www-bcf.usc.edu/~gareth/ISL/Advertising.csv', index_col=0)

# or, you can read data as DataFrame from local file system.

advertising = pd.read_csv('../Data/Advertising.csv', usecols=[1,2,3,4])

advertising.head() # advertising.tail()

| TV | Radio | Newspaper | Sales | |

|---|---|---|---|---|

| 0 | 230.1 | 37.8 | 69.2 | 22.1 |

| 1 | 44.5 | 39.3 | 45.1 | 10.4 |

| 2 | 17.2 | 45.9 | 69.3 | 9.3 |

| 3 | 151.5 | 41.3 | 58.5 | 18.5 |

| 4 | 180.8 | 10.8 | 58.4 | 12.9 |

type(advertising)

pandas.core.frame.DataFrame

advertising.shape

(200, 4)

- 200 개의 row (레코드, observation, sample)이 있음. Column은 4 개

advertising.index , advertising.columns # row index, column names

(RangeIndex(start=0, stop=200, step=1), Index(['TV', 'Radio', 'Newspaper', 'Sales'], dtype='object'))

advertising.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 200 entries, 0 to 199 Data columns (total 4 columns): TV 200 non-null float64 Radio 200 non-null float64 Newspaper 200 non-null float64 Sales 200 non-null float64 dtypes: float64(4) memory usage: 6.3 KB

데이터에 대한 자세한 정보 제공 : 타입, shape, 각 feature/column의 속성

- 자주 사용하기 바람

st(advertising) # R의 str() 같이 동작하도록 만든 간단한 함수

<class 'pandas.core.frame.DataFrame'> : dimension of (200, 4) Index: 0, 1, 2, 3, 4, 5, 6, 7, 8, 9 ... : int64 TV float64 [[230.1, 44.5, 17.2, 151.5, 180.8, 8.7, 57.5, ... Radio float64 [[37.8, 39.3, 45.9, 41.3, 10.8, 48.9, 32.8, 19... Newspaper float64 [[69.2, 45.1, 69.3, 58.5, 58.4, 75.0, 23.5, 11... Sales float64 [[22.1, 10.4, 9.3, 18.5, 12.9, 7.2, 11.8, 13.2...

간단한 Exploratory Analysis: 모델링을 하기 전에 데이터의 특성을 살펴본다¶

# seaborne 패키지를 이용해 feature들의 scatter plot을 본다

seaborn.pairplot(advertising)

<seaborn.axisgrid.PairGrid at 0x7f2b161a6ac8>

# 'Sales'와 feature들간의 관계만을 scatterplot으로 나타내고,

# R의 ggplot에서와 같이 regression line과 95% 신뢰대역을 나타내도록 함 ('kind='reg').

seaborn.pairplot(data=advertising, x_vars=['TV', 'Radio', 'Newspaper'], y_vars=['Sales'], size=6, aspect=0.8, kind='reg')

<seaborn.axisgrid.PairGrid at 0x7f2b130b5e80>

Corrplot(advertising).plot(fontsize='large') # R style Corrplot

plt.show()

Computing correlation

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/matplotlib/cbook.py:136: MatplotlibDeprecationWarning: The axisbg attribute was deprecated in version 2.0. Use facecolor instead. warnings.warn(message, mplDeprecation, stacklevel=1)

- Sales와 TV간 *강한 정비례* 관계가 있다

3.1 Simple Linear Regression : feature가 1개¶

$Y = \beta_0 + \beta_1X$

- $Y$ : response/output/target

- $X$ : feature/input/predictor

- $\beta_0$ is the intercept

- $\beta_1$ is the coefficient for $X$

Response(Y)로 sales, 1개의 feature(X)를 TV로 삼으면,

$sales = \beta_0 + \beta_1TV$

- $\beta_0$ 와 $\beta_1$ 들을 model coefficients (또는 weight) 라 함

- simple linear regression의 학습 : sales와 TV 관계에 가장 맞는(RSS를 최소화하는) 선형식을 구성하는 $\beta_0$와 $\beta_1$을 데이터를 보고 학습해 추정한다

Estimating the Coefficients of Linear Model¶

*Statsmodels* 을 사용해 advertising 데이터에 대한 linear regression 모델의 coefficient 추정

statsmodels version 0.5 부터 R 스타일 formula 형태 추가¶

Statsmodels의 Linear Model 사용하기¶

- 모델 import : 우리는 위에서 이미 "import statsmodels.formula.api as smf" 하여 관련 모듈(api)를 'smf' 라는 alias로 가져옴

- 모델 instantiate : 클래스 생성자를 이용해 모델을 만듬. 이 때 argument로 regression formula 포함

- 학습 시킴 : instantiate된 모델 객체에게 fit() 명령을 내려 학습/훈련시키고, 학습된 모델을 반환 받음

- 학습된 모델 활용 : 학습된 모델을 이용해 새로운 입력에 대해 예측을 하던가 등, 적절한 일거리를 줌

# 1. 모델 import : 모델을 포함하는 모듈을 이미 import 했음

# 2. Model Instantiation: Ordinary Least Squares (ols) 방식 linear regression 모델 만들기

# - 입력 데이터는 DataFrame 타입

lm = smf.ols(formula='Sales ~ TV', data=advertising)

# 'advertising' DataFrame에서 'Sales' column을 response로, 'TV' column을 feature로 하는

# linear regression 모델을 정의함

# 3. 모델에게 학습 시키고, 그 결과인 (학습된) 모델을 'lm_learned'으로 받음

lm_learned = lm.fit()

# 학습된 모델의 coefficients

lm_learned.params

# lm_learned.pvalues # p values

# lm_learned.rsquared # R-squared statistic

Intercept 7.032594 TV 0.047537 dtype: float64

- lm_learned._Tab_를 쳐서 'lm_learned' 객체에 어떤 method를 쓸 수 있는 지 보도록

# 보통은 위 2 & 3번 과정을 연결(chaining)함

lm = smf.ols(formula='Sales ~ TV', data=advertising).fit()

# 학습한 모델 (즉, fit model)이 만들어졌음

print ("Coeffients:\n%s \n\np-values:\n%s , \n\nr-squared: %s " % (lm.params, lm.pvalues, lm.rsquared))

Coeffients: Intercept 7.032594 TV 0.047537 dtype: float64 p-values: Intercept 1.406300e-35 TV 1.467390e-42 dtype: float64 , r-squared: 0.61187505085

다음 두 개의 cell은 response와 feature간의 관계를 시각화하는 또 다른 예¶

# Sales를 Y-축에, TV 광고비를 X-축에 놓은 scatter plot을 그리자

plt.scatter(advertising.TV, advertising.Sales)

plt.xlabel("TV (in 1000's)")

plt.ylabel("Sales (in 1000's)")

# 위 plot에 simple regression 선을 overlay

X = pd.DataFrame({'TV':[advertising.TV.min(), advertising.TV.max()]})

Y_pred = lm.predict(X)

plt.plot(X, Y_pred, c='red')

plt.title("Simple Linar Regression")

<matplotlib.text.Text at 0x7f2b108feef0>

# seaborn 패키지를 이용할 수도

seaborn.regplot(advertising.TV, advertising.Sales, order=1, ci=None, scatter_kws={'color':'r'})

plt.xlim(-50,350)

plt.ylim(ymin=0)

plt.grid()

lm.summary() # 모델 전체 요약. R의 summary() 함수와 비슷

| Dep. Variable: | Sales | R-squared: | 0.612 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.610 |

| Method: | Least Squares | F-statistic: | 312.1 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 1.47e-42 |

| Time: | 01:26:39 | Log-Likelihood: | -519.05 |

| No. Observations: | 200 | AIC: | 1042. |

| Df Residuals: | 198 | BIC: | 1049. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 7.0326 | 0.458 | 15.360 | 0.000 | 6.130 7.935 |

| TV | 0.0475 | 0.003 | 17.668 | 0.000 | 0.042 0.053 |

| Omnibus: | 0.531 | Durbin-Watson: | 1.935 |

|---|---|---|---|

| Prob(Omnibus): | 0.767 | Jarque-Bera (JB): | 0.669 |

| Skew: | -0.089 | Prob(JB): | 0.716 |

| Kurtosis: | 2.779 | Cond. No. | 338. |

# ISLR - Table 3.1

lm.summary().tables[1]

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 7.0326 | 0.458 | 15.360 | 0.000 | 6.130 7.935 |

| TV | 0.0475 | 0.003 | 17.668 | 0.000 | 0.042 0.053 |

st(advertising)

<class 'pandas.core.frame.DataFrame'> : dimension of (200, 4) Index: 0, 1, 2, 3, 4, 5, 6, 7, 8, 9 ... : int64 TV float64 [[230.1, 44.5, 17.2, 151.5, 180.8, 8.7, 57.5, ... Radio float64 [[37.8, 39.3, 45.9, 41.3, 10.8, 48.9, 32.8, 19... Newspaper float64 [[69.2, 45.1, 69.3, 58.5, 58.4, 75.0, 23.5, 11... Sales float64 [[22.1, 10.4, 9.3, 18.5, 12.9, 7.2, 11.8, 13.2...

학습된 모델 활용: 예측과 관련 이슈 들¶

- 위에서 만든 모델 lm은 Advertising의 TV 변수만을 feature로 사용해 만들었음

- 위의 R-squared 값 0.612 이나 Residual은 모델을 만들 때 사용한 데이터 (Training set)를 이용해 구한 Training Performance

- 예측분석의 목표는 training set에 대해 좋은 성능을 보이는 모델을 만듬이 아니라, 처음 보게 될 (미래)의 out-of-sample 데이터에 대해 좋은 성능을 보일 것 같은 모델을 만드는 것 (즉, generalize 잘 하여 out-of-sample 성능이 좋은 모델)

- 미래의 데이터가 지금 존재하지 않는데 현재의 모델이 미래에 어떻게 동작할 지 짐작할 수 있을까? -> 모델 평가

예측 : 만들어진 모델 (lm)을 이용해 새로운 predictor 값 (TV)을 줄 때 'Sales' 예측은?¶

- 가령, TV = 100 일 때 Sales 예측

# statsmodel formula 인터페이스는 입력을 pandas의 DataFrame 같은 array 형태 데이터 구조로 주어야 함

x_new = pd.DataFrame({'TV': [100]}) # dictionary로 df를 만드는 일반 방법

# x_new.info()

x_new.head()

| TV | |

|---|---|

| 0 | 100 |

4. 예측 : 아래에서와 같이 'predict' 메소드를 이용¶

- ** predict() 의 입력이 DataFrame 같이 array 형태로 training에 사용했던 feature들을 갖고 있어야 함**

lm.predict(x_new) # 결과인 예측치를 numpy의 ndarray로 반환

array([ 11.78625759])

손으로 계산하여 확인하면;¶

$$y = \beta_0 + \beta_1x$$$$y = 7.0326 + 0.0475 \times x$$sales_manual = lm.params.Intercept + lm.params.TV * 100

print("Manual Calculation : %6f" % sales_manual)

Manual Calculation : 11.786258

X_new = pd.DataFrame({'TV': [100, 422, 74]}) # TV가 100, 422, 또는 74일때 Sales 예측은?

lm.predict(X_new)

array([ 11.78625759, 27.09305581, 10.55030494])

Multiple Linear Regression¶

multiple linear regression: 여러 feature들을 사용해 response 추정

$Y = \beta_0 + \beta_1X_1 + ... + \beta_nX_n$

*Advertising*의 TV, Radio, Newspaper들을 feature로 하고, Sales를 response로 한 multiple linear regression :

$Sales = \beta_0 + \beta_1 \times TV + \beta_2 \times Radio + \beta_3 \times Newspaper$

lm_mul = smf.ols(formula='Sales ~ TV + Radio + Newspaper', data=advertising).fit()

lm_mul.summary()

| Dep. Variable: | Sales | R-squared: | 0.897 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.896 |

| Method: | Least Squares | F-statistic: | 570.3 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 1.58e-96 |

| Time: | 01:26:39 | Log-Likelihood: | -386.18 |

| No. Observations: | 200 | AIC: | 780.4 |

| Df Residuals: | 196 | BIC: | 793.6 |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 2.9389 | 0.312 | 9.422 | 0.000 | 2.324 3.554 |

| TV | 0.0458 | 0.001 | 32.809 | 0.000 | 0.043 0.049 |

| Radio | 0.1885 | 0.009 | 21.893 | 0.000 | 0.172 0.206 |

| Newspaper | -0.0010 | 0.006 | -0.177 | 0.860 | -0.013 0.011 |

| Omnibus: | 60.414 | Durbin-Watson: | 2.084 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 151.241 |

| Skew: | -1.327 | Prob(JB): | 1.44e-33 |

| Kurtosis: | 6.332 | Cond. No. | 454. |

결과 해석¶

- F statistic의 p-value가 매우 작으므로 (1.58e-96) 모델은 유효 (최소한 1개 이상의 variable이 response와 관련)

- TV와 Radio의 p-value는 의미있음. 하지만 Newspaper의 p-value는 0.86에 달하므로 "Newspaper가 response와 관련이 없다"라는 null-hypothesis를 거부할 수 없음. 따라서 Newspaper 변수를 모델에 포함하기에는 적합하지 않음

- R-squared가 0.89로 simple linear regression (0.612) 때보다 증가. 이 모델이 최소한 simple linear regression 보다 traning set의 response를 더 잘 설명(예측)한다고 생각할 수 있음.

- 주의: 이 R-squared는 모델을 만들 때 데이터 (즉, training set에)에 대해서 구한 것이기에 실제 환경에서도 (out-of-sample) 더 좋은 특성을 보이는 지는 확신할 수 없음

- Cross-validation와 같은 평가 방법을 통해 모델이 out-of-sample에 대해서도 generalize 잘 할까 짐작해 볼 수 있음 --> 나중에

lm_mul.summary().tables[1] # Table 3.4 of ISLR

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 2.9389 | 0.312 | 9.422 | 0.000 | 2.324 3.554 |

| TV | 0.0458 | 0.001 | 32.809 | 0.000 | 0.043 0.049 |

| Radio | 0.1885 | 0.009 | 21.893 | 0.000 | 0.172 0.206 |

| Newspaper | -0.0010 | 0.006 | -0.177 | 0.860 | -0.013 0.011 |

advertising.corr() # Table 3.5 of ISLR : correlation matrix (상관 관계)

| TV | Radio | Newspaper | Sales | |

|---|---|---|---|---|

| TV | 1.000000 | 0.054809 | 0.056648 | 0.782224 |

| Radio | 0.054809 | 1.000000 | 0.354104 | 0.576223 |

| Newspaper | 0.056648 | 0.354104 | 1.000000 | 0.228299 |

| Sales | 0.782224 | 0.576223 | 0.228299 | 1.000000 |

# Load 'credit' data from local file system

credit = pd.read_csv('../Data/Credit.csv', usecols=list(range(1,12)))

credit.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 400 entries, 0 to 399 Data columns (total 11 columns): Income 400 non-null float64 Limit 400 non-null int64 Rating 400 non-null int64 Cards 400 non-null int64 Age 400 non-null int64 Education 400 non-null int64 Gender 400 non-null object Student 400 non-null object Married 400 non-null object Ethnicity 400 non-null object Balance 400 non-null int64 dtypes: float64(1), int64(6), object(4) memory usage: 34.5+ KB

- 위 feature들의 data type (dtypes)에서 float64, int64와 같이 숫자가 아닌 'object' 인 것들은 대부분 string 또는 다른 클래스 타입. 이것들이 category 타입 변수일 가능성 많음.

- Feature중 Gender, Student, Married, Ethnicity 변수가 qualitative(categorical) 변수

- 400개의 row/observation이 있는데, 모든 feature들이 400 개의 non-null 값을 지님. 즉, missing value가 없음

credit.head(3)

| Income | Limit | Rating | Cards | Age | Education | Gender | Student | Married | Ethnicity | Balance | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 14.891 | 3606 | 283 | 2 | 34 | 11 | Male | No | Yes | Caucasian | 333 |

| 1 | 106.025 | 6645 | 483 | 3 | 82 | 15 | Female | Yes | Yes | Asian | 903 |

| 2 | 104.593 | 7075 | 514 | 4 | 71 | 11 | Male | No | No | Asian | 580 |

credit.isnull().sum() # 다시 missing value 없음을 확인

Income 0 Limit 0 Rating 0 Cards 0 Age 0 Education 0 Gender 0 Student 0 Married 0 Ethnicity 0 Balance 0 dtype: int64

seaborn.pairplot(credit[['Balance','Age','Cards','Education','Income','Limit','Rating']]) # ISLR - Fig 3.6

# 실행 시간이 조금 걸림. Wait.

<seaborn.axisgrid.PairGrid at 0x7f2b10893c88>

Corrplot(credit[['Balance','Age','Cards','Education','Income','Limit','Rating']]).plot(fontsize='large')

plt.show()

Computing correlation

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/matplotlib/cbook.py:136: MatplotlibDeprecationWarning: The axisbg attribute was deprecated in version 2.0. Use facecolor instead. warnings.warn(message, mplDeprecation, stacklevel=1)

Interpreting the *corrplot*

- 파란색(붉은색)으로 갈수록 Positive(Negative) Correlation

- 긹죽한 타원형태가 될수록 correlation이 강함

credit.Gender.unique() # Gender 변수는 단 2개의 category를 갖음

array([' Male', 'Female'], dtype=object)

카테고리형 변수 'Gender'를 feature로 활용¶

lm_cat = smf.ols(formula='Balance ~ Gender', data=credit).fit() # Gender has 2 levels -> 1 dummy variable

lm_cat.summary().tables[1] # ISLR - Table 3.7

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 509.8031 | 33.128 | 15.389 | 0.000 | 444.675 574.931 |

| Gender[T.Female] | 19.7331 | 46.051 | 0.429 | 0.669 | -70.801 110.267 |

# Regression of Balance onto Ethnicity

lm_cat_Eth = smf.ols('Balance ~ Ethnicity', credit).fit()

lm_cat_Eth.summary() # Table 3.8

| Dep. Variable: | Balance | R-squared: | 0.000 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | -0.005 |

| Method: | Least Squares | F-statistic: | 0.04344 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 0.957 |

| Time: | 01:26:49 | Log-Likelihood: | -3019.3 |

| No. Observations: | 400 | AIC: | 6045. |

| Df Residuals: | 397 | BIC: | 6057. |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 531.0000 | 46.319 | 11.464 | 0.000 | 439.939 622.061 |

| Ethnicity[T.Asian] | -18.6863 | 65.021 | -0.287 | 0.774 | -146.515 109.142 |

| Ethnicity[T.Caucasian] | -12.5025 | 56.681 | -0.221 | 0.826 | -123.935 98.930 |

| Omnibus: | 28.829 | Durbin-Watson: | 1.946 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 27.395 |

| Skew: | 0.581 | Prob(JB): | 1.13e-06 |

| Kurtosis: | 2.460 | Cond. No. | 4.39 |

- F-statistic p-value가 0.957에 달해 'Balance와 Ethnicity간 관련이 없다'는 null hypothesis를 거부할 수 없기에 이 데이터에 따르면 null hypothesis를 따른는 것이 좋다. 즉, 이 모델은 꽝!

st(credit)

<class 'pandas.core.frame.DataFrame'> : dimension of (400, 11) Index: 0, 1, 2, 3, 4, 5, 6, 7, 8, 9 ... : int64 Income float64 [[14.890999999999998, 106.025, 104.59299999999... Limit int64 [[3606, 6645, 7075, 9504, 4897, 8047, 3388, 71... Rating int64 [[283, 483, 514, 681, 357, 569, 259, 512, 266,... Cards int64 [[2, 3, 4, 5, 1, 6, 7]] Age int64 [[34, 82, 71, 36, 68, 77, 37, 87, 66, 41, 30, ... Education int64 [[11, 15, 16, 10, 12, 9, 13, 19, 14, 7, 17, 8,... Gender object [[ Male, Female]] Student object [[No, Yes]] Married object [[Yes, No]] Ethnicity object [[Caucasian, Asian, African American]] Balance int64 [[333, 903, 580, 964, 331, 1151, 203, 872, 279...

변수들 중 'Ethnicity'만 제외하려면 - formula에 feature 다 나열하기 귀찮음. 뒤에...

lm_all = smf.ols('Balance ~ Income + Limit + Rating + Cards + Age + Education + Gender + Student + Married', credit).fit()

lm_all.summary()

| Dep. Variable: | Balance | R-squared: | 0.955 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.954 |

| Method: | Least Squares | F-statistic: | 918.2 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 2.49e-256 |

| Time: | 01:26:49 | Log-Likelihood: | -2399.4 |

| No. Observations: | 400 | AIC: | 4819. |

| Df Residuals: | 390 | BIC: | 4859. |

| Df Model: | 9 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | -468.4037 | 34.355 | -13.634 | 0.000 | -535.948 -400.859 |

| Gender[T.Female] | -10.4067 | 9.904 | -1.051 | 0.294 | -29.879 9.065 |

| Student[T.Yes] | 426.4692 | 16.678 | 25.571 | 0.000 | 393.680 459.259 |

| Married[T.Yes] | -7.0191 | 10.278 | -0.683 | 0.495 | -27.226 13.188 |

| Income | -7.8020 | 0.234 | -33.349 | 0.000 | -8.262 -7.342 |

| Limit | 0.1931 | 0.033 | 5.909 | 0.000 | 0.129 0.257 |

| Rating | 1.1023 | 0.489 | 2.253 | 0.025 | 0.140 2.064 |

| Cards | 17.9233 | 4.332 | 4.137 | 0.000 | 9.406 26.441 |

| Age | -0.6347 | 0.293 | -2.164 | 0.031 | -1.211 -0.058 |

| Education | -1.1150 | 1.596 | -0.699 | 0.485 | -4.253 2.023 |

| Omnibus: | 34.234 | Durbin-Watson: | 1.958 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 40.854 |

| Skew: | 0.775 | Prob(JB): | 1.34e-09 |

| Kurtosis: | 3.217 | Cond. No. | 3.68e+04 |

Removing the Additive Assumptions : 변수간 Interaction¶

# TV와 Radio간 interaction term을 주고 linear model을 만들면

lm_interact = smf.ols('Sales ~ TV + Radio + TV:Radio', advertising).fit()

lm_interact.summary().tables[1] # Table 3.9

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 6.7502 | 0.248 | 27.233 | 0.000 | 6.261 7.239 |

| TV | 0.0191 | 0.002 | 12.699 | 0.000 | 0.016 0.022 |

| Radio | 0.0289 | 0.009 | 3.241 | 0.001 | 0.011 0.046 |

| TV:Radio | 0.0011 | 5.24e-05 | 20.727 | 0.000 | 0.001 0.001 |

- TV와 Radio간 interaction이 유효

smf.ols('Sales ~ TV*Radio', advertising).fit().summary().tables[1] # 앞의 formula를 이렇게 표현 가능

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 6.7502 | 0.248 | 27.233 | 0.000 | 6.261 7.239 |

| TV | 0.0191 | 0.002 | 12.699 | 0.000 | 0.016 0.022 |

| Radio | 0.0289 | 0.009 | 3.241 | 0.001 | 0.011 0.046 |

| TV:Radio | 0.0011 | 5.24e-05 | 20.727 | 0.000 | 0.001 0.001 |

smf.ols('Sales ~ TV + Newspaper*Radio', advertising).fit().summary()

| Dep. Variable: | Sales | R-squared: | 0.897 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.895 |

| Method: | Least Squares | F-statistic: | 426.6 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 3.25e-95 |

| Time: | 01:26:50 | Log-Likelihood: | -385.95 |

| No. Observations: | 200 | AIC: | 781.9 |

| Df Residuals: | 195 | BIC: | 798.4 |

| Df Model: | 4 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 3.1467 | 0.437 | 7.193 | 0.000 | 2.284 4.009 |

| TV | 0.0458 | 0.001 | 32.746 | 0.000 | 0.043 0.049 |

| Newspaper | -0.0094 | 0.014 | -0.688 | 0.492 | -0.036 0.018 |

| Radio | 0.1801 | 0.015 | 11.930 | 0.000 | 0.150 0.210 |

| Newspaper:Radio | 0.0003 | 0.000 | 0.678 | 0.498 | -0.001 0.001 |

| Omnibus: | 60.978 | Durbin-Watson: | 2.098 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 151.663 |

| Skew: | -1.344 | Prob(JB): | 1.17e-33 |

| Kurtosis: | 6.313 | Cond. No. | 4.59e+03 |

- Newspaper와 Radio간 interaction은 유효하지 않음

Interaction between qualitative variable and a quantitative variable¶

# Income(quantitative) 과 Student(qualitative with 2 levels)간 Interaction이 없다하고 모델을 학습하면;

lm_no_interact = smf.ols('Balance ~ Income + Student', credit).fit()

lm_no_interact.summary()

| Dep. Variable: | Balance | R-squared: | 0.277 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.274 |

| Method: | Least Squares | F-statistic: | 76.22 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 9.64e-29 |

| Time: | 01:26:50 | Log-Likelihood: | -2954.4 |

| No. Observations: | 400 | AIC: | 5915. |

| Df Residuals: | 397 | BIC: | 5927. |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 211.1430 | 32.457 | 6.505 | 0.000 | 147.333 274.952 |

| Student[T.Yes] | 382.6705 | 65.311 | 5.859 | 0.000 | 254.272 511.069 |

| Income | 5.9843 | 0.557 | 10.751 | 0.000 | 4.890 7.079 |

| Omnibus: | 119.719 | Durbin-Watson: | 1.951 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 23.617 |

| Skew: | 0.252 | Prob(JB): | 7.44e-06 |

| Kurtosis: | 1.922 | Cond. No. | 192. |

# Income(quantitative) 과 Studen(qualitative with 2 levels)간 Interaction이 있게 만들면;

lm_interact = smf.ols('Balance ~ Income*Student', credit).fit()

lm_interact.summary()

| Dep. Variable: | Balance | R-squared: | 0.280 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.274 |

| Method: | Least Squares | F-statistic: | 51.30 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 4.94e-28 |

| Time: | 01:26:50 | Log-Likelihood: | -2953.7 |

| No. Observations: | 400 | AIC: | 5915. |

| Df Residuals: | 396 | BIC: | 5931. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 200.6232 | 33.698 | 5.953 | 0.000 | 134.373 266.873 |

| Student[T.Yes] | 476.6758 | 104.351 | 4.568 | 0.000 | 271.524 681.827 |

| Income | 6.2182 | 0.592 | 10.502 | 0.000 | 5.054 7.382 |

| Income:Student[T.Yes] | -1.9992 | 1.731 | -1.155 | 0.249 | -5.403 1.404 |

| Omnibus: | 107.788 | Durbin-Watson: | 1.952 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 22.158 |

| Skew: | 0.228 | Prob(JB): | 1.54e-05 |

| Kurtosis: | 1.941 | Cond. No. | 309. |

- 'Income'과 'Student' 사이의 interaction이 없다고 생각하는 것이 옳으며, 이는 R-square 값이 거의 증가하지 않은 것을 통해서도 짐작할 수 있다.

Non-linear relationships using polynomial regressions¶

# load 'Auto' data

auto = pd.read_csv('../Data/Auto.csv')

auto.info()

auto.head()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 397 entries, 0 to 396 Data columns (total 9 columns): mpg 397 non-null float64 cylinders 397 non-null int64 displacement 397 non-null float64 horsepower 397 non-null object weight 397 non-null int64 acceleration 397 non-null float64 year 397 non-null int64 origin 397 non-null int64 name 397 non-null object dtypes: float64(3), int64(4), object(2) memory usage: 28.0+ KB

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | name | |

|---|---|---|---|---|---|---|---|---|---|

| 0 | 18.0 | 8 | 307.0 | 130 | 3504 | 12.0 | 70 | 1 | chevrolet chevelle malibu |

| 1 | 15.0 | 8 | 350.0 | 165 | 3693 | 11.5 | 70 | 1 | buick skylark 320 |

| 2 | 18.0 | 8 | 318.0 | 150 | 3436 | 11.0 | 70 | 1 | plymouth satellite |

| 3 | 16.0 | 8 | 304.0 | 150 | 3433 | 12.0 | 70 | 1 | amc rebel sst |

| 4 | 17.0 | 8 | 302.0 | 140 | 3449 | 10.5 | 70 | 1 | ford torino |

(중요) horsepower 변수가 숫자이어야 함. 그런데, 위의 auto.info()로 본 horsepower 변수 타입이 'object'로 되어 있음. 즉 숫자가 아니라고 함. auto.head()로 보니 처음에는 분명 숫자. 따라서 horsepower 변수 중간 어디 즈음 숫자가 아닌 것이 있음

# Find out which rows have non-numeric value on 'horsepower' column

auto_problem = auto[auto.horsepower.apply(lambda x: not(x.isnumeric()))]

auto_problem

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | name | |

|---|---|---|---|---|---|---|---|---|---|

| 32 | 25.0 | 4 | 98.0 | ? | 2046 | 19.0 | 71 | 1 | ford pinto |

| 126 | 21.0 | 6 | 200.0 | ? | 2875 | 17.0 | 74 | 1 | ford maverick |

| 330 | 40.9 | 4 | 85.0 | ? | 1835 | 17.3 | 80 | 2 | renault lecar deluxe |

| 336 | 23.6 | 4 | 140.0 | ? | 2905 | 14.3 | 80 | 1 | ford mustang cobra |

| 354 | 34.5 | 4 | 100.0 | ? | 2320 | 15.8 | 81 | 2 | renault 18i |

5개의 observation 들이 'horsepower' feature에 숫자가 아님. 원본 auto.csv 를 보고 확인

- 위의 row들을 제거할 수도 있고, 또는 파일을 읽을 때 위의 문제가 있는 row들을 제거하고 읽을 수도 있음

# Read the data again. This time skipping problematic rows

auto = pd.read_csv('../Data/Auto.csv', na_values='?').dropna()

auto.info()

auto.iloc[28: 34, :]

<class 'pandas.core.frame.DataFrame'> Int64Index: 392 entries, 0 to 396 Data columns (total 9 columns): mpg 392 non-null float64 cylinders 392 non-null int64 displacement 392 non-null float64 horsepower 392 non-null float64 weight 392 non-null int64 acceleration 392 non-null float64 year 392 non-null int64 origin 392 non-null int64 name 392 non-null object dtypes: float64(4), int64(4), object(1) memory usage: 30.6+ KB

| mpg | cylinders | displacement | horsepower | weight | acceleration | year | origin | name | |

|---|---|---|---|---|---|---|---|---|---|

| 28 | 9.0 | 8 | 304.0 | 193.0 | 4732 | 18.5 | 70 | 1 | hi 1200d |

| 29 | 27.0 | 4 | 97.0 | 88.0 | 2130 | 14.5 | 71 | 3 | datsun pl510 |

| 30 | 28.0 | 4 | 140.0 | 90.0 | 2264 | 15.5 | 71 | 1 | chevrolet vega 2300 |

| 31 | 25.0 | 4 | 113.0 | 95.0 | 2228 | 14.0 | 71 | 3 | toyota corona |

| 33 | 19.0 | 6 | 232.0 | 100.0 | 2634 | 13.0 | 71 | 1 | amc gremlin |

| 34 | 16.0 | 6 | 225.0 | 105.0 | 3439 | 15.5 | 71 | 1 | plymouth satellite custom |

- 문제있는 row들이 제거됨을 확인

mpg를 $horsepower$ 와 $horsepower^2$ 에 대해 regression¶

# OLS regression of mpg onto horsepower and squared(horsepower)

lm_quadratic = smf.ols('mpg ~ horsepower + np.square(horsepower)', data=auto).fit()

lm_quadratic.summary().tables[1] # ISLR - Table 3.10

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 56.9001 | 1.800 | 31.604 | 0.000 | 53.360 60.440 |

| horsepower | -0.4662 | 0.031 | -14.978 | 0.000 | -0.527 -0.405 |

| np.square(horsepower) | 0.0012 | 0.000 | 10.080 | 0.000 | 0.001 0.001 |

# Polynomial regression upto 3'rd degree

lm_deg3 = smf.ols('mpg ~ horsepower + np.power(horsepower,2) + np.power(horsepower,3)', data=auto).fit()

lm_deg3.summary()

| Dep. Variable: | mpg | R-squared: | 0.688 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.686 |

| Method: | Least Squares | F-statistic: | 285.5 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 8.41e-98 |

| Time: | 01:26:50 | Log-Likelihood: | -1132.8 |

| No. Observations: | 392 | AIC: | 2274. |

| Df Residuals: | 388 | BIC: | 2289. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 60.6848 | 4.563 | 13.298 | 0.000 | 51.713 69.657 |

| horsepower | -0.5689 | 0.118 | -4.824 | 0.000 | -0.801 -0.337 |

| np.power(horsepower, 2) | 0.0021 | 0.001 | 2.193 | 0.029 | 0.000 0.004 |

| np.power(horsepower, 3) | -2.147e-06 | 2.38e-06 | -0.903 | 0.367 | -6.82e-06 2.53e-06 |

| Omnibus: | 16.987 | Durbin-Watson: | 1.094 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 34.528 |

| Skew: | 0.204 | Prob(JB): | 3.18e-08 |

| Kurtosis: | 4.395 | Cond. No. | 5.53e+07 |

- R의 poly()같은 함수 만드는 것은 쉬움. 함수로 만들 가치 없음 .

3.6 Lab: Linear Regression¶

sanity check¶

Boston = pd.read_table("../Data/Boston.csv", sep=',')

st(Boston)

Boston.head()

<class 'pandas.core.frame.DataFrame'> : dimension of (506, 14) Index: 0, 1, 2, 3, 4, 5, 6, 7, 8, 9 ... : int64 crim float64 [[0.00632, 0.02731, 0.02729, 0.03237, 0.06905,... zn float64 [[18.0, 0.0, 12.5, 75.0, 21.0, 90.0, 85.0, 100... indus float64 [[2.31, 7.07, 2.18, 7.87, 8.14, 5.96, 2.95, 6.... chas int64 [[0.0]] nox float64 [[0.538, 0.469, 0.458, 0.524, 0.499, 0.428, 0.... rm float64 [[6.575, 6.421, 7.185, 6.998, 7.147, 6.43, 6.0... age float64 [[65.2, 78.9, 61.1, 45.8, 54.2, 58.7, 66.6, 96... dis float64 [[4.09, 4.9671, 6.0622, 5.5605, 5.9505, 6.0821... rad int64 [[1.0, 2.0, 3.0, 5.0, 4.0, 8.0]] tax int64 [[296.0, 242.0, 222.0, 311.0, 307.0, 279.0, 25... ptratio float64 [[15.3, 17.8, 18.7, 15.2, 21.0, 19.2, 18.3, 17... black float64 [[396.9, 392.83, 394.63, 394.12, 395.6, 386.63... lstat float64 [[4.98, 9.14, 4.03, 2.94, 5.33, 5.21, 12.43, 1... medv float64 [[24.0, 21.6, 34.7, 33.4, 36.2, 28.7, 22.9, 27...

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | black | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 396.90 | 4.98 | 24.0 |

| 1 | 0.02731 | 0.0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 396.90 | 9.14 | 21.6 |

| 2 | 0.02729 | 0.0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 392.83 | 4.03 | 34.7 |

| 3 | 0.03237 | 0.0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 394.63 | 2.94 | 33.4 |

| 4 | 0.06905 | 0.0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 396.90 | 5.33 | 36.2 |

- 모든 column들이 숫자(numeric) 임

Boston.describe()

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | black | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| count | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 | 506.000000 |

| mean | 3.613524 | 11.363636 | 11.136779 | 0.069170 | 0.554695 | 6.284634 | 68.574901 | 3.795043 | 9.549407 | 408.237154 | 18.455534 | 356.674032 | 12.653063 | 22.532806 |

| std | 8.601545 | 23.322453 | 6.860353 | 0.253994 | 0.115878 | 0.702617 | 28.148861 | 2.105710 | 8.707259 | 168.537116 | 2.164946 | 91.294864 | 7.141062 | 9.197104 |

| min | 0.006320 | 0.000000 | 0.460000 | 0.000000 | 0.385000 | 3.561000 | 2.900000 | 1.129600 | 1.000000 | 187.000000 | 12.600000 | 0.320000 | 1.730000 | 5.000000 |

| 25% | 0.082045 | 0.000000 | 5.190000 | 0.000000 | 0.449000 | 5.885500 | 45.025000 | 2.100175 | 4.000000 | 279.000000 | 17.400000 | 375.377500 | 6.950000 | 17.025000 |

| 50% | 0.256510 | 0.000000 | 9.690000 | 0.000000 | 0.538000 | 6.208500 | 77.500000 | 3.207450 | 5.000000 | 330.000000 | 19.050000 | 391.440000 | 11.360000 | 21.200000 |

| 75% | 3.677082 | 12.500000 | 18.100000 | 0.000000 | 0.624000 | 6.623500 | 94.075000 | 5.188425 | 24.000000 | 666.000000 | 20.200000 | 396.225000 | 16.955000 | 25.000000 |

| max | 88.976200 | 100.000000 | 27.740000 | 1.000000 | 0.871000 | 8.780000 | 100.000000 | 12.126500 | 24.000000 | 711.000000 | 22.000000 | 396.900000 | 37.970000 | 50.000000 |

Boston.isnull().sum()

crim 0 zn 0 indus 0 chas 0 nox 0 rm 0 age 0 dis 0 rad 0 tax 0 ptratio 0 black 0 lstat 0 medv 0 dtype: int64

Boston.columns # pandas DataFrame 클래스는 'columns' attribute을 갖고 있음

Index(['crim', 'zn', 'indus', 'chas', 'nox', 'rm', 'age', 'dis', 'rad', 'tax',

'ptratio', 'black', 'lstat', 'medv'],

dtype='object')

3.6.2 medv를 response, lstat를 predictor로 한 simple regression¶

lm_fit = smf.ols(formula='medv ~ lstat', data=Boston).fit()

lm_fit.summary()

| Dep. Variable: | medv | R-squared: | 0.544 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.543 |

| Method: | Least Squares | F-statistic: | 601.6 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 5.08e-88 |

| Time: | 01:26:51 | Log-Likelihood: | -1641.5 |

| No. Observations: | 506 | AIC: | 3287. |

| Df Residuals: | 504 | BIC: | 3295. |

| Df Model: | 1 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 34.5538 | 0.563 | 61.415 | 0.000 | 33.448 35.659 |

| lstat | -0.9500 | 0.039 | -24.528 | 0.000 | -1.026 -0.874 |

| Omnibus: | 137.043 | Durbin-Watson: | 0.892 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 291.373 |

| Skew: | 1.453 | Prob(JB): | 5.36e-64 |

| Kurtosis: | 5.319 | Cond. No. | 29.7 |

lm_fit.resid.describe() # Residuals statistics

count 5.060000e+02 mean 1.832877e-14 std 6.209603e+00 min -1.516745e+01 25% -3.989612e+00 50% -1.318186e+00 75% 2.033701e+00 max 2.450013e+01 dtype: float64

*** 신뢰구간 ***

lm_fit.conf_int(alpha=0.05) # default alpha=0.05 : 95% confidence interval

| 0 | 1 | |

|---|---|---|

| Intercept | 33.448457 | 35.659225 |

| lstat | -1.026148 | -0.873951 |

참고 : OLS Prediction with confidence interval

from statsmodels.sandbox.regression.predstd import wls_prediction_std

X_new = pd.DataFrame({'lstat':[5,10,15]})

lm_fit.predict(X_new)

array([ 29.80359411, 25.05334734, 20.30310057])

plt.scatter(Boston.lstat, Boston.medv )

X = pd.DataFrame({'lstat':[Boston.lstat.min(), Boston.lstat.max()]})

Y_pred = lm_fit.predict(X)

plt.plot(X, Y_pred, c='red')

plt.xlabel("lstat")

plt.ylabel("medv")

<matplotlib.text.Text at 0x7f2b01d2aa58>

3.6.3 Multiple Linear Regression¶

lm_fit = smf.ols('medv ~ lstat+age', data=Boston).fit()

lm_fit.summary()

| Dep. Variable: | medv | R-squared: | 0.551 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.549 |

| Method: | Least Squares | F-statistic: | 309.0 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 2.98e-88 |

| Time: | 01:26:51 | Log-Likelihood: | -1637.5 |

| No. Observations: | 506 | AIC: | 3281. |

| Df Residuals: | 503 | BIC: | 3294. |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 33.2228 | 0.731 | 45.458 | 0.000 | 31.787 34.659 |

| lstat | -1.0321 | 0.048 | -21.416 | 0.000 | -1.127 -0.937 |

| age | 0.0345 | 0.012 | 2.826 | 0.005 | 0.011 0.059 |

| Omnibus: | 124.288 | Durbin-Watson: | 0.945 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 244.026 |

| Skew: | 1.362 | Prob(JB): | 1.02e-53 |

| Kurtosis: | 5.038 | Cond. No. | 201. |

R의 "formula = medv ~ ." 같이 medv를 제외한 다른 모든 column을 predictor로 삼는 간편 식이 python에 없음. 그냥 다음과 같이 하면 됨.¶

# Response인 'medv'를 제외한 모든 column들을 feature로 삼으려면,

columns_selected = "+".join(Boston.columns.difference(["medv"]))

my_formula = "medv ~ " + columns_selected

my_formula

'medv ~ age+black+chas+crim+dis+indus+lstat+nox+ptratio+rad+rm+tax+zn'

- 단순 조작이기에 함수로 만들 필요 없겠죠... 참고로, formula에서 R 처럼 '-'도 먹힘

lm_fit = smf.ols(formula = my_formula, data=Boston).fit()

lm_fit.summary()

| Dep. Variable: | medv | R-squared: | 0.741 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.734 |

| Method: | Least Squares | F-statistic: | 108.1 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 6.72e-135 |

| Time: | 01:26:52 | Log-Likelihood: | -1498.8 |

| No. Observations: | 506 | AIC: | 3026. |

| Df Residuals: | 492 | BIC: | 3085. |

| Df Model: | 13 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 36.4595 | 5.103 | 7.144 | 0.000 | 26.432 46.487 |

| age | 0.0007 | 0.013 | 0.052 | 0.958 | -0.025 0.027 |

| black | 0.0093 | 0.003 | 3.467 | 0.001 | 0.004 0.015 |

| chas | 2.6867 | 0.862 | 3.118 | 0.002 | 0.994 4.380 |

| crim | -0.1080 | 0.033 | -3.287 | 0.001 | -0.173 -0.043 |

| dis | -1.4756 | 0.199 | -7.398 | 0.000 | -1.867 -1.084 |

| indus | 0.0206 | 0.061 | 0.334 | 0.738 | -0.100 0.141 |

| lstat | -0.5248 | 0.051 | -10.347 | 0.000 | -0.624 -0.425 |

| nox | -17.7666 | 3.820 | -4.651 | 0.000 | -25.272 -10.262 |

| ptratio | -0.9527 | 0.131 | -7.283 | 0.000 | -1.210 -0.696 |

| rad | 0.3060 | 0.066 | 4.613 | 0.000 | 0.176 0.436 |

| rm | 3.8099 | 0.418 | 9.116 | 0.000 | 2.989 4.631 |

| tax | -0.0123 | 0.004 | -3.280 | 0.001 | -0.020 -0.005 |

| zn | 0.0464 | 0.014 | 3.382 | 0.001 | 0.019 0.073 |

| Omnibus: | 178.041 | Durbin-Watson: | 1.078 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 783.126 |

| Skew: | 1.521 | Prob(JB): | 8.84e-171 |

| Kurtosis: | 8.281 | Cond. No. | 1.51e+04 |

lm_fit.resid.describe() # Residuals statistics

count 5.060000e+02 mean -3.845813e-13 std 4.683822e+00 min -1.559447e+01 25% -2.729716e+00 50% -5.180489e-01 75% 1.777051e+00 max 2.619927e+01 dtype: float64

# 'age' 를 제외한 다른 모든 변수들을 predictor로 삼으려면

columns_selected = "+".join(Boston.columns.difference(["medv", "age"]))

my_formula = "medv ~ " + columns_selected

lm_fit1 = smf.ols(formula = my_formula, data=Boston).fit()

lm_fit1.summary().tables[1]

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 36.4369 | 5.080 | 7.172 | 0.000 | 26.456 46.418 |

| black | 0.0093 | 0.003 | 3.481 | 0.001 | 0.004 0.015 |

| chas | 2.6890 | 0.860 | 3.128 | 0.002 | 1.000 4.378 |

| crim | -0.1080 | 0.033 | -3.290 | 0.001 | -0.173 -0.043 |

| dis | -1.4786 | 0.191 | -7.757 | 0.000 | -1.853 -1.104 |

| indus | 0.0206 | 0.061 | 0.335 | 0.738 | -0.100 0.141 |

| lstat | -0.5239 | 0.048 | -10.999 | 0.000 | -0.617 -0.430 |

| nox | -17.7135 | 3.679 | -4.814 | 0.000 | -24.943 -10.484 |

| ptratio | -0.9522 | 0.130 | -7.308 | 0.000 | -1.208 -0.696 |

| rad | 0.3058 | 0.066 | 4.627 | 0.000 | 0.176 0.436 |

| rm | 3.8144 | 0.408 | 9.338 | 0.000 | 3.012 4.617 |

| tax | -0.0123 | 0.004 | -3.283 | 0.001 | -0.020 -0.005 |

| zn | 0.0463 | 0.014 | 3.404 | 0.001 | 0.020 0.073 |

lm_fit1.resid.describe()

count 5.060000e+02 mean 2.973818e-14 std 4.683835e+00 min -1.560538e+01 25% -2.731276e+00 50% -5.187814e-01 75% 1.760098e+00 max 2.622427e+01 dtype: float64

3.6.4 Interaction Terms¶

lm_fit = smf.ols('medv ~ lstat*age', data=Boston).fit()

lm_fit.summary()

| Dep. Variable: | medv | R-squared: | 0.556 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.553 |

| Method: | Least Squares | F-statistic: | 209.3 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 4.86e-88 |

| Time: | 01:26:52 | Log-Likelihood: | -1635.0 |

| No. Observations: | 506 | AIC: | 3278. |

| Df Residuals: | 502 | BIC: | 3295. |

| Df Model: | 3 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 36.0885 | 1.470 | 24.553 | 0.000 | 33.201 38.976 |

| lstat | -1.3921 | 0.167 | -8.313 | 0.000 | -1.721 -1.063 |

| age | -0.0007 | 0.020 | -0.036 | 0.971 | -0.040 0.038 |

| lstat:age | 0.0042 | 0.002 | 2.244 | 0.025 | 0.001 0.008 |

| Omnibus: | 135.601 | Durbin-Watson: | 0.965 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 296.955 |

| Skew: | 1.417 | Prob(JB): | 3.29e-65 |

| Kurtosis: | 5.461 | Cond. No. | 6.88e+03 |

Boston.head()

| crim | zn | indus | chas | nox | rm | age | dis | rad | tax | ptratio | black | lstat | medv | |

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 0.00632 | 18.0 | 2.31 | 0 | 0.538 | 6.575 | 65.2 | 4.0900 | 1 | 296 | 15.3 | 396.90 | 4.98 | 24.0 |

| 1 | 0.02731 | 0.0 | 7.07 | 0 | 0.469 | 6.421 | 78.9 | 4.9671 | 2 | 242 | 17.8 | 396.90 | 9.14 | 21.6 |

| 2 | 0.02729 | 0.0 | 7.07 | 0 | 0.469 | 7.185 | 61.1 | 4.9671 | 2 | 242 | 17.8 | 392.83 | 4.03 | 34.7 |

| 3 | 0.03237 | 0.0 | 2.18 | 0 | 0.458 | 6.998 | 45.8 | 6.0622 | 3 | 222 | 18.7 | 394.63 | 2.94 | 33.4 |

| 4 | 0.06905 | 0.0 | 2.18 | 0 | 0.458 | 7.147 | 54.2 | 6.0622 | 3 | 222 | 18.7 | 396.90 | 5.33 | 36.2 |

임의의 test set을 만들어 response를 예측해 봄¶

# Interaction term이 있지만 이는 'age'와 'lstat' 변수에서 파생된 것이기에 이 두 변수만 필요함

test = pd.DataFrame({'age':[65.4, 79, 23], 'lstat':[4.8, 10, 5]})

test

| age | lstat | |

|---|---|---|

| 0 | 65.4 | 4.8 |

| 1 | 79.0 | 10.0 |

| 2 | 23.0 | 5.0 |

lm_fit.predict(exog=test)

array([ 30.66386729, 25.39362159, 29.58930643])

- "predict()의 'exog' 같은 단어들은 어디서 유래했을까" 가 궁금하면 여기로

# residual 을 계산해 봄. 모델을 fit할 때 사용하지 않은 변수인 'rm'을 예측 변수로 넣어도 에러 발생 않함

y_predict = lm_fit.predict(Boston.loc[:,['age', 'lstat', 'rm']]) # training set에 대한 prediction

(Boston.medv - y_predict)[0:5]

0 -6.458215 1 -4.704760 2 3.242407 3 0.877696 4 6.369921 Name: medv, dtype: float64

lm_fit.resid[:5] # 위의 결과와 같음

0 -6.458215 1 -4.704760 2 3.242407 3 0.877696 4 6.369921 dtype: float64

# lm_fit.predict(Boston.loc[:,['age', 'rm']])

# 'lstat'이 없다고 exception 일으킴

3.6.5 Non-linear Transformation of the Predictors¶

lm_fit2 = smf.ols('medv ~ lstat + np.power(lstat, 2)', data=Boston).fit()

lm_fit2.summary()

| Dep. Variable: | medv | R-squared: | 0.641 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.639 |

| Method: | Least Squares | F-statistic: | 448.5 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 1.56e-112 |

| Time: | 01:26:53 | Log-Likelihood: | -1581.3 |

| No. Observations: | 506 | AIC: | 3169. |

| Df Residuals: | 503 | BIC: | 3181. |

| Df Model: | 2 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 42.8620 | 0.872 | 49.149 | 0.000 | 41.149 44.575 |

| lstat | -2.3328 | 0.124 | -18.843 | 0.000 | -2.576 -2.090 |

| np.power(lstat, 2) | 0.0435 | 0.004 | 11.628 | 0.000 | 0.036 0.051 |

| Omnibus: | 107.006 | Durbin-Watson: | 0.921 |

|---|---|---|---|

| Prob(Omnibus): | 0.000 | Jarque-Bera (JB): | 228.388 |

| Skew: | 1.128 | Prob(JB): | 2.55e-50 |

| Kurtosis: | 5.397 | Cond. No. | 1.13e+03 |

import statsmodels.api as sm

lm_fit = smf.ols('medv ~ lstat', data=Boston).fit()

table = sm.stats.anova_lm(lm_fit, lm_fit2, typ=1)

print(table)

df_resid ssr df_diff ss_diff F Pr(>F) 0 504.0 19472.381418 0.0 NaN NaN NaN 1 503.0 15347.243158 1.0 4125.13826 135.199822 7.630116e-28

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/scipy/stats/_distn_infrastructure.py:875: RuntimeWarning: invalid value encountered in greater return (self.a < x) & (x < self.b) /home/lee/Programs/anaconda3/lib/python3.6/site-packages/scipy/stats/_distn_infrastructure.py:875: RuntimeWarning: invalid value encountered in less return (self.a < x) & (x < self.b) /home/lee/Programs/anaconda3/lib/python3.6/site-packages/scipy/stats/_distn_infrastructure.py:1814: RuntimeWarning: invalid value encountered in less_equal cond2 = cond0 & (x <= self.a)

3.6.6 Qualitative Predictors¶

Carseats = pd.read_csv("../Data/Carseats.csv", index_col=0)

Carseats.head()

| Sales | CompPrice | Income | Advertising | Population | Price | ShelveLoc | Age | Education | Urban | US | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 9.50 | 138 | 73 | 11 | 276 | 120 | Bad | 42 | 17 | Yes | Yes |

| 2 | 11.22 | 111 | 48 | 16 | 260 | 83 | Good | 65 | 10 | Yes | Yes |

| 3 | 10.06 | 113 | 35 | 10 | 269 | 80 | Medium | 59 | 12 | Yes | Yes |

| 4 | 7.40 | 117 | 100 | 4 | 466 | 97 | Medium | 55 | 14 | Yes | Yes |

| 5 | 4.15 | 141 | 64 | 3 | 340 | 128 | Bad | 38 | 13 | Yes | No |

Carseats.columns

Index(['Sales', 'CompPrice', 'Income', 'Advertising', 'Population', 'Price',

'ShelveLoc', 'Age', 'Education', 'Urban', 'US'],

dtype='object')

Carseats.info()

<class 'pandas.core.frame.DataFrame'> Int64Index: 400 entries, 1 to 400 Data columns (total 11 columns): Sales 400 non-null float64 CompPrice 400 non-null int64 Income 400 non-null int64 Advertising 400 non-null int64 Population 400 non-null int64 Price 400 non-null int64 ShelveLoc 400 non-null object Age 400 non-null int64 Education 400 non-null int64 Urban 400 non-null object US 400 non-null object dtypes: float64(1), int64(7), object(3) memory usage: 37.5+ KB

columns_selected = "+".join(Carseats.columns.difference(["Sales"]))

my_formula = "Sales ~ Income:Advertising + Price:Age + " + columns_selected

my_formula

'Sales ~ Income:Advertising + Price:Age + Advertising+Age+CompPrice+Education+Income+Population+Price+ShelveLoc+US+Urban'

lm_fit = smf.ols(my_formula, data=Carseats).fit()

lm_fit.summary()

| Dep. Variable: | Sales | R-squared: | 0.876 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.872 |

| Method: | Least Squares | F-statistic: | 210.0 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 6.14e-166 |

| Time: | 01:26:53 | Log-Likelihood: | -564.67 |

| No. Observations: | 400 | AIC: | 1157. |

| Df Residuals: | 386 | BIC: | 1213. |

| Df Model: | 13 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 6.5756 | 1.009 | 6.519 | 0.000 | 4.592 8.559 |

| ShelveLoc[T.Good] | 4.8487 | 0.153 | 31.724 | 0.000 | 4.548 5.149 |

| ShelveLoc[T.Medium] | 1.9533 | 0.126 | 15.531 | 0.000 | 1.706 2.201 |

| US[T.Yes] | -0.1576 | 0.149 | -1.058 | 0.291 | -0.450 0.135 |

| Urban[T.Yes] | 0.1402 | 0.112 | 1.247 | 0.213 | -0.081 0.361 |

| Income:Advertising | 0.0008 | 0.000 | 2.698 | 0.007 | 0.000 0.001 |

| Price:Age | 0.0001 | 0.000 | 0.801 | 0.424 | -0.000 0.000 |

| Advertising | 0.0702 | 0.023 | 3.107 | 0.002 | 0.026 0.115 |

| Age | -0.0579 | 0.016 | -3.633 | 0.000 | -0.089 -0.027 |

| CompPrice | 0.0929 | 0.004 | 22.567 | 0.000 | 0.085 0.101 |

| Education | -0.0209 | 0.020 | -1.063 | 0.288 | -0.059 0.018 |

| Income | 0.0109 | 0.003 | 4.183 | 0.000 | 0.006 0.016 |

| Population | 0.0002 | 0.000 | 0.433 | 0.665 | -0.001 0.001 |

| Price | -0.1008 | 0.007 | -13.549 | 0.000 | -0.115 -0.086 |

| Omnibus: | 1.281 | Durbin-Watson: | 2.047 |

|---|---|---|---|

| Prob(Omnibus): | 0.527 | Jarque-Bera (JB): | 1.147 |

| Skew: | 0.129 | Prob(JB): | 0.564 |

| Kurtosis: | 3.050 | Cond. No. | 1.31e+05 |

Carseats.head()

| Sales | CompPrice | Income | Advertising | Population | Price | ShelveLoc | Age | Education | Urban | US | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 1 | 9.50 | 138 | 73 | 11 | 276 | 120 | Bad | 42 | 17 | Yes | Yes |

| 2 | 11.22 | 111 | 48 | 16 | 260 | 83 | Good | 65 | 10 | Yes | Yes |

| 3 | 10.06 | 113 | 35 | 10 | 269 | 80 | Medium | 59 | 12 | Yes | Yes |

| 4 | 7.40 | 117 | 100 | 4 | 466 | 97 | Medium | 55 | 14 | Yes | Yes |

| 5 | 4.15 | 141 | 64 | 3 | 340 | 128 | Bad | 38 | 13 | Yes | No |

Carseats_training = Carseats.loc[:,'CompPrice':]

# Carseats_training

lm_fit.predict(Carseats_training)[:5] # training set feature를 이용해 training set response 추정

array([ 7.25155178, 12.22190446, 9.17309518, 8.44242764, 6.06916727])

(Carseats.Sales - lm_fit.predict(Carseats_training)).describe() # residual statistics w.r.t. training set

count 4.000000e+02 mean -2.958256e-12 std 9.940033e-01 min -2.920817e+00 25% -7.502943e-01 50% 1.767764e-02 75% 6.754104e-01 max 3.341301e+00 Name: Sales, dtype: float64

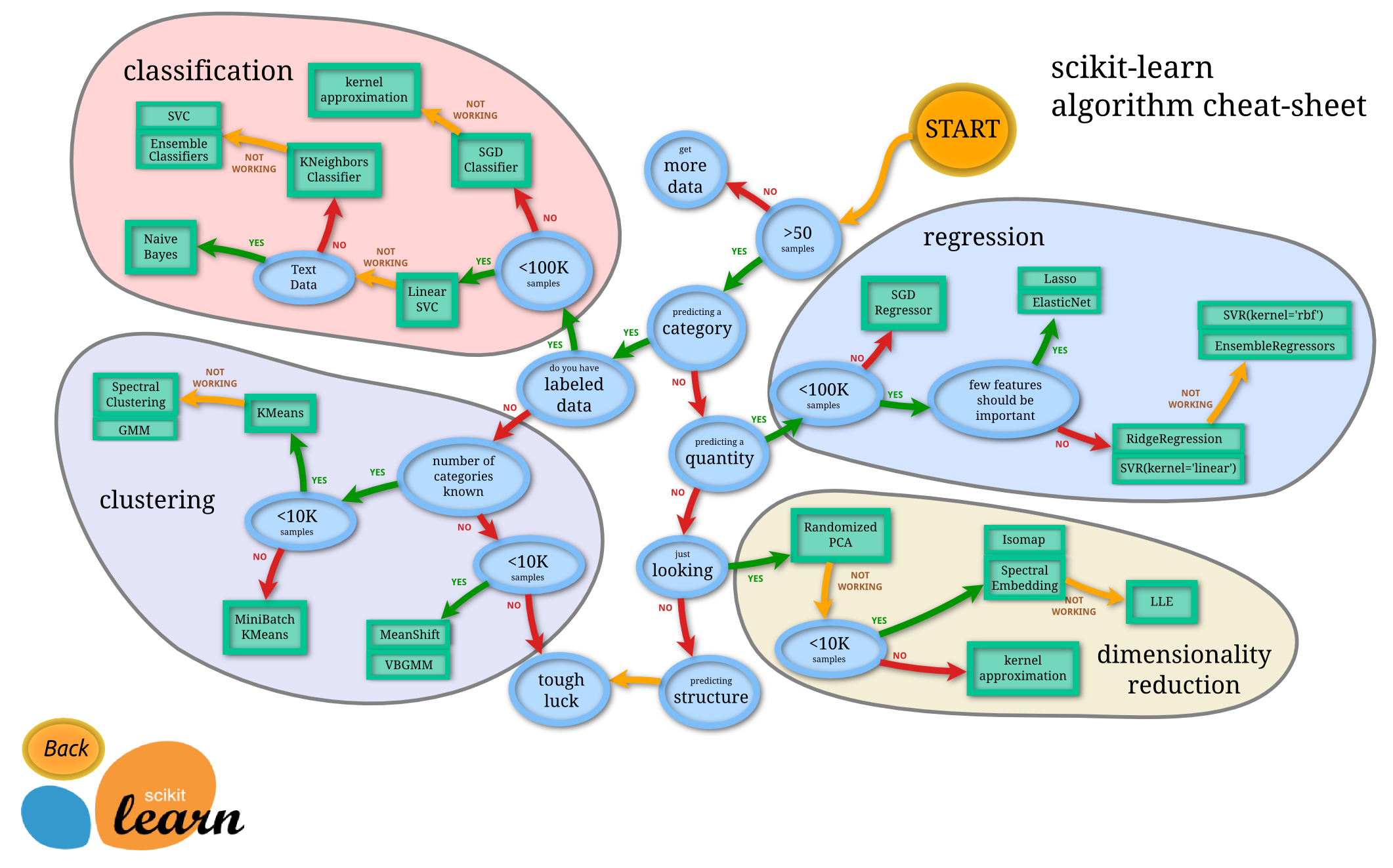

Scikit-learn이 지원하는 머신러닝 알고리즘 및 적합한 알고리즘 선택 요령¶

scikit-learn Linear Regression¶

말 그대로 가장 밋밋한 Linear Regression 알고리즘인 Ordinary Least Squares Linear Regression 연습 - 3장의 Linear Regression 내용은 이것으로 다 됨¶

간략 scikit-learn 소개¶

- 학습 모델(알고리즘)을 estimator 라 함. 정확한 정의는: an estimator is a Python object that implements the methods fit(X, y) and predict(T)

scikit-learn의 estimator들은 데이터에 대해 다음과 같은 조건을 요구함¶

- feature와 response가 각각 독립적인 객체

- feature와 response가 숫자

- feature와 response가 NumPy ndarray이거나 또는 DataFrame, Python array같이 쉽게 ndarray로 변환 가능 해야 함. 또한, scipy의 sparse matrix를 허용.

- feature는 2-D ndarray로 shape가 (n_samples, n_features) 이어야 함. Response는 'n_samples' 길이의 vector 이어야 함.

scikit-learn의 estimator 사용 패턴¶

1. estimator를 import¶

- *from sklearn.linear_model import LinearRegression*

2. instantiate the estimator¶

- *model = LinearRegression()* : instantiate할 때 estimator에서 hyperparameter를 지정해 튜닝

3. estimator에게 데이터(X:feature, y:response)를 제공해 학습시킴 (모델 traing/fit¶

- *model.fit(X, y) * : fit가 in-place 진행, 즉 결과가 model 내부에 저장됨

4. 학습된 estimator에 새로운 데이터의 feature(X_new)를 주고 response를 추정¶

- *y_predict = model.predict(X_new) *

Advertising 데이터를 이용¶

1. Estimator (여기서는 'LinearRegression')을 갖고 옴¶

from sklearn.linear_model import LinearRegression # sklearn : scikit-learn 을 말함

# from sklearn import datasets

'LinearRegression' estimator가 쓸 수 있도록 data 구조 만들기¶

advertising.head()

| TV | Radio | Newspaper | Sales | |

|---|---|---|---|---|

| 0 | 230.1 | 37.8 | 69.2 | 22.1 |

| 1 | 44.5 | 39.3 | 45.1 | 10.4 |

| 2 | 17.2 | 45.9 | 69.3 | 9.3 |

| 3 | 151.5 | 41.3 | 58.5 | 18.5 |

| 4 | 180.8 | 10.8 | 58.4 | 12.9 |

advertising.info()

<class 'pandas.core.frame.DataFrame'> RangeIndex: 200 entries, 0 to 199 Data columns (total 4 columns): TV 200 non-null float64 Radio 200 non-null float64 Newspaper 200 non-null float64 Sales 200 non-null float64 dtypes: float64(4) memory usage: 6.3 KB

- Sales를 response, 나머지 TV, Radio, Newspaper를 feature 삼으려 함

- response와 feature들이 모두 숫자 --> scikit-learn의 data 조건-2 만족

# X 와 y 각각 만들기

X = advertising.loc[ :, ['TV', 'Radio', 'Newspaper'] ] # DataFrame 타입

y = advertising.Sales

print(X.head(), '\n')

print(X.values[:5], '\n')

print(type(X.values))

TV Radio Newspaper 0 230.1 37.8 69.2 1 44.5 39.3 45.1 2 17.2 45.9 69.3 3 151.5 41.3 58.5 4 180.8 10.8 58.4 [[ 230.1 37.8 69.2] [ 44.5 39.3 45.1] [ 17.2 45.9 69.3] [ 151.5 41.3 58.5] [ 180.8 10.8 58.4]] <class 'numpy.ndarray'>

- pandas의 DataFrame 객체는 데이터를 numpy.ndarray 형태로 내부에 갖고 있다

X.shape , X.values.shape # DataFrame X의 모양, 내부 ndarray의 모양이 같음

((200, 3), (200, 3))

type(y)

pandas.core.series.Series

y.head()

0 22.1 1 10.4 2 9.3 3 18.5 4 12.9 Name: Sales, dtype: float64

y.values

array([ 22.1, 10.4, 9.3, 18.5, 12.9, 7.2, 11.8, 13.2, 4.8,

10.6, 8.6, 17.4, 9.2, 9.7, 19. , 22.4, 12.5, 24.4,

11.3, 14.6, 18. , 12.5, 5.6, 15.5, 9.7, 12. , 15. ,

15.9, 18.9, 10.5, 21.4, 11.9, 9.6, 17.4, 9.5, 12.8,

25.4, 14.7, 10.1, 21.5, 16.6, 17.1, 20.7, 12.9, 8.5,

14.9, 10.6, 23.2, 14.8, 9.7, 11.4, 10.7, 22.6, 21.2,

20.2, 23.7, 5.5, 13.2, 23.8, 18.4, 8.1, 24.2, 15.7,

14. , 18. , 9.3, 9.5, 13.4, 18.9, 22.3, 18.3, 12.4,

8.8, 11. , 17. , 8.7, 6.9, 14.2, 5.3, 11. , 11.8,

12.3, 11.3, 13.6, 21.7, 15.2, 12. , 16. , 12.9, 16.7,

11.2, 7.3, 19.4, 22.2, 11.5, 16.9, 11.7, 15.5, 25.4,

17.2, 11.7, 23.8, 14.8, 14.7, 20.7, 19.2, 7.2, 8.7,

5.3, 19.8, 13.4, 21.8, 14.1, 15.9, 14.6, 12.6, 12.2,

9.4, 15.9, 6.6, 15.5, 7. , 11.6, 15.2, 19.7, 10.6,

6.6, 8.8, 24.7, 9.7, 1.6, 12.7, 5.7, 19.6, 10.8,

11.6, 9.5, 20.8, 9.6, 20.7, 10.9, 19.2, 20.1, 10.4,

11.4, 10.3, 13.2, 25.4, 10.9, 10.1, 16.1, 11.6, 16.6,

19. , 15.6, 3.2, 15.3, 10.1, 7.3, 12.9, 14.4, 13.3,

14.9, 18. , 11.9, 11.9, 8. , 12.2, 17.1, 15. , 8.4,

14.5, 7.6, 11.7, 11.5, 27. , 20.2, 11.7, 11.8, 12.6,

10.5, 12.2, 8.7, 26.2, 17.6, 22.6, 10.3, 17.3, 15.9,

6.7, 10.8, 9.9, 5.9, 19.6, 17.3, 7.6, 9.7, 12.8,

25.5, 13.4])

type(y.values)

numpy.ndarray

# y.values.head() # error. 이유는 head()는 pandas DataFrame, Series 메소드. numpy.ndarray에 안됨

y.values[:5]

array([ 22.1, 10.4, 9.3, 18.5, 12.9])

y.shape

(200,)

y.values.shape # pandas and numpy classes both support shape() method

(200,)

DataFrame과 Series는 데이터를 내부에서 numpy.ndarray로 관리.¶

- *** scikit-learn estimator들은 DataFrame과 Series 데이터 구조도 받아드린다***

2. Estimator를 instantiate¶

model = LinearRegression()

3. Estimator를 훈련¶

model.fit(X, y)

LinearRegression(copy_X=True, fit_intercept=True, n_jobs=1, normalize=False)

학습된 Estimator 살펴보기 :¶

- model.[Tab] 을 하여 어떤 메소드가 있는 지 보자

print(model.coef_) # feature matrix 'X'의 feature 순서대로, 즉 TV', 'Radio', 'Newspaper'

list(zip(X.columns, model.coef_ ))

[ 0.04576465 0.18853002 -0.00103749]

[('TV', 0.045764645455397587),

('Radio', 0.18853001691820459),

('Newspaper', -0.0010374930424762452)]

- 앞에 statsmodels linear model의 결과와 같음

model.intercept_

2.9388893694594085

model.residues_ # Residual sum of squares (RSS). 0.18에 생겼는데 0.19에 deprecate

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/sklearn/utils/deprecation.py:70: DeprecationWarning: Function residues_ is deprecated; ``residues_`` is deprecated and will be removed in 0.19 warnings.warn(msg, category=DeprecationWarning)

556.82526290218698

- scikit-learn에서 coef_, intercept_ 같이 estimator attribute명 뒤에 '_'가 붙은 것은 (학습된) 모델의 attribute임을 나타냄. 따라서 학습되지 않은 estimator에 위 멤버를 요청하면 에러

model.score(X, y, sample_weight=None) # R-squared

0.89721063817895208

4. Predict (예측/추정) : response 추정¶

- 앞 단계에서 estimator가 훈련을 통해 학습이 됨

- 이 estimator로 feature가 입력될 때 response를 추정해 본다

# training 할 때 사용한 X를 그대로 feature로 삼아 response를 보자

y_pred = model.predict(X)

pd.DataFrame({'y_True': y, "y_pred": y_pred}).head(10)

| y_True | y_pred | |

|---|---|---|

| 0 | 22.1 | 20.523974 |

| 1 | 10.4 | 12.337855 |

| 2 | 9.3 | 12.307671 |

| 3 | 18.5 | 17.597830 |

| 4 | 12.9 | 13.188672 |

| 5 | 7.2 | 12.478348 |

| 6 | 11.8 | 11.729760 |

| 7 | 13.2 | 12.122953 |

| 8 | 4.8 | 3.727341 |

| 9 | 10.6 | 12.550849 |

# RSS manual 계산과 비교

np.square(y - y_pred).sum(), model.residues_

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/sklearn/utils/deprecation.py:70: DeprecationWarning: Function residues_ is deprecated; ``residues_`` is deprecated and will be removed in 0.19 warnings.warn(msg, category=DeprecationWarning)

(556.8252629021873, 556.82526290218698)

X.tail()

| TV | Radio | Newspaper | |

|---|---|---|---|

| 195 | 38.2 | 3.7 | 13.8 |

| 196 | 94.2 | 4.9 | 8.1 |

| 197 | 177.0 | 9.3 | 6.4 |

| 198 | 283.6 | 42.0 | 66.2 |

| 199 | 232.1 | 8.6 | 8.7 |

X.values[-5:]

array([[ 38.2, 3.7, 13.8],

[ 94.2, 4.9, 8.1],

[ 177. , 9.3, 6.4],

[ 283.6, 42. , 66.2],

[ 232.1, 8.6, 8.7]])

기본적으로 predict 메소드의 입력 feature는 numpy ndarray이어야 함¶

X_new = np.array([[45.4, 12, 44]]) # One observation with features TV, Radio, Newspaper order

X_new.shape

(1, 3)

- X_new가 2D ndarray 이어야 함. X_new는 1x3 array. column 배열이 estimator를 훈련시킬 때의 X column 순서와 같아야 함

새로운 feature에 대한 response 추정¶

model.predict(X_new)

array([ 7.23331478])

predict()는 입력 feature로 DataFrame과 Python array도 잘 받아드린다. 단 2D 이어야 함¶

X_new = pd.DataFrame([[45.4, 12, 44]])

model.predict(X_new) # OK

array([ 7.23331478])

X_new = [[45.4, 12, 44]]

model.predict(X_new) # OK

array([ 7.23331478])

X_new

[[45.4, 12, 44]]

X_new = [45.4, 12, 44]

model.predict(X_new) # 아직은 됨. 곧 에러로 취급한다고. 2D array로 만드라는 말

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/sklearn/utils/validation.py:395: DeprecationWarning: Passing 1d arrays as data is deprecated in 0.17 and will raise ValueError in 0.19. Reshape your data either using X.reshape(-1, 1) if your data has a single feature or X.reshape(1, -1) if it contains a single sample. DeprecationWarning)

array([ 7.23331478])

X_new = pd.Series([45.4, 12, 44]) # 위와 같은 주의

model.predict(X_new)

/home/lee/Programs/anaconda3/lib/python3.6/site-packages/sklearn/utils/validation.py:395: DeprecationWarning: Passing 1d arrays as data is deprecated in 0.17 and will raise ValueError in 0.19. Reshape your data either using X.reshape(-1, 1) if your data has a single feature or X.reshape(1, -1) if it contains a single sample. DeprecationWarning)

array([ 7.23331478])

X_new = pd.DataFrame({'TV':[34,44,56], 'Radio':[123,55,23], 'Newspaper':[23,40,121]})

X_new

| Newspaper | Radio | TV | |

|---|---|---|---|

| 0 | 23 | 123 | 34 |

| 1 | 40 | 55 | 44 |

| 2 | 121 | 23 | 56 |

# 내부 ndarray를 보면,

X_new.values

array([[ 23, 123, 34],

[ 40, 55, 44],

[121, 23, 56]])

X_new의 column 순서가 처음 X_new를 dictionary로 만들 때의 순서와 다름. 이는 Python Dictionary가 순서 개념이 없기 때문임. 원래 순서 TV, Radio, Newspaper 순으로 순서를 맞추어 predict() 메소드에 주어야 함¶

X.columns

Index(['TV', 'Radio', 'Newspaper'], dtype='object')

X_new = X_new[X.columns] # X_new의 column 순서를 X 순서에 따라 재배열 함

X_new.values

array([[ 34, 123, 23],

[ 44, 55, 40],

[ 56, 23, 121]])

model.predict(X_new)

array([ 27.66021706, 15.28018498, 9.71236325])

[Lesson] predict()에게 주는 데이터를 만드는 등, 중요한 ndarray를 만들 경우 녀석이 내가 생각했던 그대로 되어있나 확인하자¶

*Note*

scikit-learn OLS API reference 에 있듯이 이 estimator는 F-statitic, p-value, confidence interval 등을 기본 제공하지 않음. 또한, statsmodels과 같이 categorical 변수, interaction, 변수를 non-linear (polynomial) 변환 적용 등이 공짜가 아님.

물론, 이런 모든 것들을 변수들을 미리 preprocessing 하여 가능함. statsmodels이나 R의 모델들은 categorical feature가 있을 시 자동적으로 preprocessing 해 준 것임.

scikit-learn과 Python 생태계는 매우 다양하고 강력한 preprocessing library/기능을 제공함.

이 estimator를 파생/확장하여 categoric 변수지원, interaction 지원, F-statitic, p-value, confidence interval 등을 제공하는 것은 쉬우나 이는 Python 이나 SW 철학에 어긋남 (공부하여, 이해하고, 인정하고, 고마와하며 갖다 쓰면 되지, 같은 것을 다시 만들 이유는 없음). 필요하면 statsmodels 쓰면 됨.

ISLR 6장에는 여기에서 배운 것의 심화 내용이 있음. 모두 어렵지 않은 내용임. 6장의 내용도 scikit-learn이 잘 지원함.

** 단순하거나, 복잡하거나, preprocessing을 어떻게 했던지 기본적으로 모든 linear 모델은 response와 feature들간에 linear한 관계가 있을 때 잘 동작함 **

동영상 참고¶

- Hastie & Tibshirani의 Ch.3 강의 : ISLR 저자들의 강의

- Kevin Markham의 scikit-learn 강의 : 쉽게, 친절하게 함

- Jake VanderPlas: Machine Learning with Scikit Learn : Linear Regression 에 관한 것은 아니나 scikit-learn 으로 iris classficiation에 관한 tutorial

- Machine Learning with Scikit Learn | SciPy 2015 Tutorial | Andreas Mueller & Kyle Kastner Part I : scikit-learn Machine Learning 전반에 관한 tutorial

- 위 강의들과 함께 있는 url들을 따라 가보도록.

마지막으로,¶

Carseats.info()

<class 'pandas.core.frame.DataFrame'> Int64Index: 400 entries, 1 to 400 Data columns (total 11 columns): Sales 400 non-null float64 CompPrice 400 non-null int64 Income 400 non-null int64 Advertising 400 non-null int64 Population 400 non-null int64 Price 400 non-null int64 ShelveLoc 400 non-null object Age 400 non-null int64 Education 400 non-null int64 Urban 400 non-null object US 400 non-null object dtypes: float64(1), int64(7), object(3) memory usage: 37.5+ KB

all_features = '+'.join(Carseats.columns.difference(['Sales']))

my_formula = "Sales ~ " + all_features + " - Population - Education + ShelveLoc:Advertising + Income:Advertising"

print("formula = ", my_formula)

lm_Carseats = smf.ols(formula = my_formula, data=Carseats).fit()

lm_Carseats.summary()

formula = Sales ~ Advertising+Age+CompPrice+Education+Income+Population+Price+ShelveLoc+US+Urban - Population - Education + ShelveLoc:Advertising + Income:Advertising

| Dep. Variable: | Sales | R-squared: | 0.876 |

|---|---|---|---|

| Model: | OLS | Adj. R-squared: | 0.872 |

| Method: | Least Squares | F-statistic: | 227.1 |

| Date: | Tue, 21 Nov 2017 | Prob (F-statistic): | 8.23e-167 |

| Time: | 01:26:57 | Log-Likelihood: | -565.42 |

| No. Observations: | 400 | AIC: | 1157. |

| Df Residuals: | 387 | BIC: | 1209. |

| Df Model: | 12 | ||

| Covariance Type: | nonrobust |

| coef | std err | t | P>|t| | [95.0% Conf. Int.] | |

|---|---|---|---|---|---|

| Intercept | 5.6339 | 0.519 | 10.849 | 0.000 | 4.613 6.655 |

| ShelveLoc[T.Good] | 4.8258 | 0.217 | 22.206 | 0.000 | 4.399 5.253 |

| ShelveLoc[T.Medium] | 2.0352 | 0.174 | 11.680 | 0.000 | 1.693 2.378 |

| US[T.Yes] | -0.1546 | 0.146 | -1.056 | 0.292 | -0.442 0.133 |

| Urban[T.Yes] | 0.1299 | 0.112 | 1.160 | 0.247 | -0.090 0.350 |

| Advertising | 0.0762 | 0.027 | 2.796 | 0.005 | 0.023 0.130 |

| ShelveLoc[T.Good]:Advertising | 0.0043 | 0.023 | 0.188 | 0.851 | -0.041 0.049 |

| ShelveLoc[T.Medium]:Advertising | -0.0114 | 0.019 | -0.594 | 0.553 | -0.049 0.026 |

| Age | -0.0458 | 0.003 | -14.406 | 0.000 | -0.052 -0.040 |

| CompPrice | 0.0931 | 0.004 | 22.634 | 0.000 | 0.085 0.101 |

| Income | 0.0109 | 0.003 | 4.207 | 0.000 | 0.006 0.016 |

| Price | -0.0952 | 0.003 | -35.929 | 0.000 | -0.100 -0.090 |

| Income:Advertising | 0.0008 | 0.000 | 2.701 | 0.007 | 0.000 0.001 |

| Omnibus: | 0.927 | Durbin-Watson: | 2.027 |

|---|---|---|---|

| Prob(Omnibus): | 0.629 | Jarque-Bera (JB): | 0.822 |

| Skew: | 0.110 | Prob(JB): | 0.663 |

| Kurtosis: | 3.034 | Cond. No. | 7.50e+03 |

print("exit with 0")

exit with 0