02 - Linear Regression¶

version 0.4, Feb 2017

Part of the Tutorial Practical Machine Learning¶

This notebook is licensed under a Creative Commons Attribution-ShareAlike 3.0 Unported License. Special thanks goes to Kevin Markham

import pandas as pd

import numpy as np

%matplotlib inline

import matplotlib.pyplot as plt

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm

import itertools

plt.style.use('fivethirtyeight')

%%javascript

IPython.OutputArea.auto_scroll_threshold = 99999;

# Test Dataset

data = pd.read_csv('data/houses_portland.csv')

data.head()

| area | bedroom | price | |

|---|---|---|---|

| 0 | 2104 | 3 | 399900 |

| 1 | 1600 | 3 | 329900 |

| 2 | 2400 | 3 | 369000 |

| 3 | 1416 | 2 | 232000 |

| 4 | 3000 | 4 | 539900 |

data.columns

Index(['area', 'bedroom', ' price'], dtype='object')

y = data[' price'].values

X = data['area'].values

plt.scatter(X, y)

plt.xlabel('Area')

plt.ylabel('Price')

<matplotlib.text.Text at 0x7f044948bd68>

y_mean, y_std = y.mean(), y.std()

X_mean, X_std = X.mean(), X.std()

y = (y - y_mean)/ y_std

X = (X - X_mean)/ X_std

plt.scatter(X, y)

plt.xlabel('Area')

plt.ylabel('Price')

<matplotlib.text.Text at 0x7f0448f473c8>

Form of linear regression¶

$$h_\beta(x) = \beta_0 + \beta_1x_1 + \beta_2x_2 + ... + \beta_nx_n$$¶

- $h_\beta(x)$ is the response

- $\beta_0$ is the intercept

- $\beta_1$ is the coefficient for $x_1$ (the first feature)

- $\beta_n$ is the coefficient for $x_n$ (the nth feature)

The $\beta$ values are called the model coefficients:

- These values are estimated (or "learned") during the model fitting process using the least squares criterion.

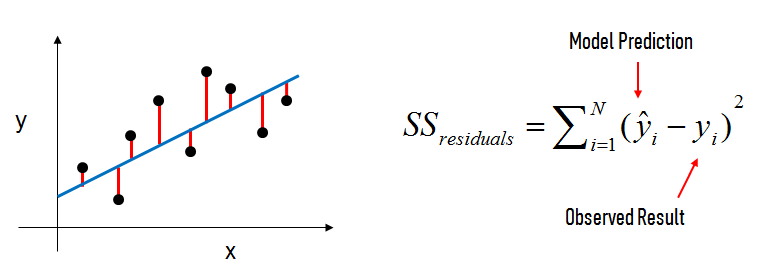

- Specifically, we are find the line (mathematically) which minimizes the sum of squared residuals (or "sum of squared errors").

- And once we've learned these coefficients, we can use the model to predict the response.

In the diagram above:

- The black dots are the observed values of x and y.

- The blue line is our least squares line.

- The red lines are the residuals, which are the vertical distances between the observed values and the least squares line.

# create X and y

n_samples = X.shape[0]

X_ = np.c_[np.ones(n_samples), X]

Lets suppose the following betas

beta_ini = np.array([-1, 1])

# h

def lr_h(beta,x):

return np.dot(beta, x.T)

# scatter plot

plt.scatter(X, y)

# Plot the linear regression

x = np.c_[np.ones(2), [X.min(), X.max()]]

plt.plot(x[:, 1], lr_h(beta_ini, x), 'r', lw=5)

plt.xlabel('Area')

plt.ylabel('Price')

<matplotlib.text.Text at 0x7f0448eb2b38>

Lets calculate the error of such regression

# Cost function

def lr_cost_func(beta, x, y):

# Can be vectorized

res = 0

for i in range(x.shape[0]):

res += (lr_h(beta,x[i, :]) - y[i]) ** 2

res *= 1 / (2*x.shape[0])

return res

lr_cost_func(beta_ini, X_, y)

0.64501240712187469

Understanding the cost function¶

Lets see how the cost function looks like for different values of $\beta$

beta0 = np.arange(-15, 20, 1)

beta1 = 2

cost_func=[]

for beta_0 in beta0:

cost_func.append(lr_cost_func(np.array([beta_0, beta1]), X_, y) )

plt.plot(beta0, cost_func)

plt.xlabel('beta_0')

plt.ylabel('J(beta)')

<matplotlib.text.Text at 0x7f0448ea1a90>

beta0 = 0

beta1 = np.arange(-15, 20, 1)

cost_func=[]

for beta_1 in beta1:

cost_func.append(lr_cost_func(np.array([beta0, beta_1]), X_, y) )

plt.plot(beta1, cost_func)

plt.xlabel('beta_1')

plt.ylabel('J(beta)')

<matplotlib.text.Text at 0x7f0448e0cb38>

Analyzing both at the same time

beta0 = np.arange(-5, 7, 0.2)

beta1 = np.arange(-5, 7, 0.2)

cost_func = pd.DataFrame(index=beta0, columns=beta1)

for beta_0 in beta0:

for beta_1 in beta1:

cost_func.ix[beta_0, beta_1] = lr_cost_func(np.array([beta_0, beta_1]), X_, y)

betas = np.transpose([np.tile(beta0, beta1.shape[0]), np.repeat(beta1, beta0.shape[0])])

fig = plt.figure(figsize=(10, 10))

ax = fig.gca(projection='3d')

ax.plot_trisurf(betas[:, 0], betas[:, 1], cost_func.T.values.flatten(), cmap=cm.jet, linewidth=0.1)

ax.set_xlabel('beta_0')

ax.set_ylabel('beta_1')

ax.set_zlabel('J(beta)')

plt.show()

It can also be seen as a contour plot

contour_levels = [0, 0.1, 0.25, 0.5, 0.75, 1, 1.5, 2, 3, 4, 5, 7, 10, 12, 15, 20]

plt.contour(beta0, beta1, cost_func.T.values, contour_levels)

plt.xlabel('beta_0')

plt.ylabel('beta_1')

<matplotlib.text.Text at 0x7f04474f56d8>

Lets understand how different values of betas are observed on the contour plot

betas = np.array([[0, 0],

[-1, -1],

[-5, 5],

[3, -2]])

for beta in betas:

print('\n\nLinear Regression with betas ', beta)

f, (ax1, ax2) = plt.subplots(1,2, figsize=(12, 6))

ax2.contour(beta0, beta1, cost_func.T.values, contour_levels)

ax2.set_xlabel('beta_0')

ax2.set_ylabel('beta_1')

ax2.scatter(beta[0], beta[1], s=50)

# scatter plot

ax1.scatter(X, y)

# Plot the linear regression

x = np.c_[np.ones(2), [X.min(), X.max()]]

ax1.plot(x[:, 1], lr_h(beta, x), 'r', lw=5)

ax1.set_xlabel('Area')

ax1.set_ylabel('Price')

plt.show()

Linear Regression with betas [0 0]

Linear Regression with betas [-1 -1]

Linear Regression with betas [-5 5]

Linear Regression with betas [ 3 -2]

Gradient descent¶

Have some function $J(\beta_0, \beta_1)$

Want $\min_{\beta_0, \beta_1}J(\beta_0, \beta_1)$

Process:

Start with some $\beta_0, \beta_1$

Keep changing $\beta_0, \beta_1$ to reduce $J(\beta_0, \beta_1)$

until hopefully end up at a minimum

For the particular case of linear regression with one variable and one intercept the gradient is calculated as:

$$\frac{\partial }{\partial \beta_j} J(\beta_0, \beta_1) = \frac{\partial }{\partial \beta_j} \frac{1}{2n}\sum_{i=1}^n (h_\beta(x_i)-y_i)^2$$¶

$$\frac{\partial }{\partial \beta_j} J(\beta_0, \beta_1) = \frac{\partial }{\partial \beta_j} \frac{1}{2n}\sum_{i=1}^n (\beta_0 + \beta_1x_i-y_i)^2$$¶

$ j = 0: \frac{\partial }{\partial \beta_0} = \frac{1}{n}\sum_{i=1}^n (\beta_0 + \beta_1x_i-y_i)$¶

$ j = 1: \frac{\partial }{\partial \beta_1} = \frac{1}{n}\sum_{i=1}^n (\beta_0 + \beta_1x_i-y_i) \cdot x_i$¶

Calculate gradient¶

# gradient calculation

beta_ini = np.array([-1.5, 0.])

def gradient(beta, x, y):

# Not vectorized

gradient_0 = 1 / x.shape[0] * ((lr_h(beta, x) - y).sum())

gradient_1 = 1 / x.shape[0] * ((lr_h(beta, x) - y)* x[:, 1]).sum()

return np.array([gradient_0, gradient_1])

gradient(beta_ini, X_, y)

array([-1.5 , -0.85498759])

Gradient descent algorithm¶

def gradient_descent(x, y, beta_ini, alpha, iters):

betas = np.zeros((iters, beta_ini.shape[0] + 1))

beta = beta_ini

for iter_ in range(iters):

betas[iter_, :-1] = beta

betas[iter_, -1] = lr_cost_func(beta, x, y)

beta -= alpha * gradient(beta, x, y)

return betas

iters = 100

alpha = 0.05

beta_ini = np.array([-4., -4.])

betas = gradient_descent(X_, y, beta_ini, alpha, iters)

Lets see the evolution of the cost per iteration

plt.plot(range(iters), betas[:, -1])

plt.xlabel('iteration')

plt.ylabel('J(beta)')

<matplotlib.text.Text at 0x7f0448e1b7f0>

Understanding what it is doing in each iteration

betas_ = betas[range(0, iters, 10), :-1]

for i, beta in enumerate(betas_):

print('\n\nLinear Regression with betas ', beta)

f, (ax1, ax2) = plt.subplots(1,2, figsize=(12, 6))

ax2.contour(beta0, beta1, cost_func.T.values, contour_levels)

ax2.set_xlabel('beta_0')

ax2.set_ylabel('beta_1')

ax2.scatter(beta[0], beta[1], c='r', s=50)

if i > 0:

for beta_ in betas_[:i]:

ax2.scatter(beta_[0], beta_[1], s=50)

# scatter plot

ax1.scatter(X, y)

# Plot the linear regression

x = np.c_[np.ones(2), [X.min(), X.max()]]

ax1.plot(x[:, 1], lr_h(beta, x), 'r', lw=5)

ax1.set_xlabel('Area')

ax1.set_ylabel('Price')

plt.show()

Linear Regression with betas [-4. -4.]

Linear Regression with betas [-2.39494776 -2.05187282]

Linear Regression with betas [-1.43394369 -0.88545711]

Linear Regression with betas [-0.85855506 -0.18708094]

Linear Regression with betas [-0.51404863 0.23106267]

Estimated Betas

betas[-1, :-1]

beta = np.dot(np.linalg.inv(np.dot(X_.T, X_)),np.dot(X_.T, y))

beta

Estimating the regression using sklearn¶

Using OLS¶

# import

from sklearn.linear_model import LinearRegression

# Initialize

linreg = LinearRegression(fit_intercept=False)

# Fit

linreg.fit(X_, y)

linreg.coef_

Using (Stochastic) Gradient Descent*¶

*Differs from normal gradient descent by updating the weights with each example. This converges faster for large datasets

# import

from sklearn.linear_model import SGDRegressor

# Initialize

linreg2 = SGDRegressor(fit_intercept=False, n_iter=100)

# Fit

linreg2.fit(X_, y)

linreg2.coef_

Comparing OLS and GD¶

| Gradient Descent | Normal Equation |

|---|---|

| Need to choose $\alpha$ | No need to choose $\alpha$ |

| Needs many iterations | Don't need to iterate |

| Works weel even when $k$ is large | Slow if $k$ is very large |

| Need to compute $(X^TX)^{-1}$ |

Linear regression with multiple variables¶

Lets create a new freature $ area^2 $

data['area2'] = data['area'] ** 2

data.head()

Notation review¶

- n = n_samples = number of examples

- k = number of features

- y = price

- $x^{(i)}$ = features of the $i$ example

i = 2

data.ix[2, ['area', 'area2']]

- $x_j^{(i)}$ = value of the $j$ feature of the $i$ example

i = 2

j = 2

data.ix[2, 'area2']

Create new matrix X and scale¶

X = data[['area', 'area2']].values

X[0:5]

from sklearn.preprocessing import StandardScaler

ss = StandardScaler(with_mean=True, with_std=True)

ss.fit(X.astype(np.float))

X = ss.transform(X.astype(np.float))

ss.mean_, ss.scale_

X[0:5]

X_ = np.c_[np.ones(n_samples), X]

X_[0:5]

Cost function¶

The goal became to estimate the parameters $\beta$ that minimize the sum of squared residuals

$$J(\beta)=\frac{1}{2n}\sum_{i=1}^n (h_\beta(x^{(i)})-y_i)^2$$¶

$$h_\beta(x^{(i)}) = \sum_{j=0}^k \beta_j x_j^{(i)}$$¶

$$J(\beta)=\frac{1}{2n}\sum_{i=1}^n \left( \left( \sum_{j=0}^k \beta_j x_j^{(i)}\right) -y_i \right)^2$$¶

Note that $x^0$ is refering to the column of ones

beta_ini = np.array([0., 0., 0.])

# gradient calculation

def gradient(beta, x, y):

return 1 / x.shape[0] * np.dot((lr_h(beta, x) - y).T, x)

gradient(beta_ini, X_, y)

beta_ini = np.array([0., 0., 0.])

alpha = 0.005

iters = 100

betas = gradient_descent(X_, y, beta_ini, alpha, iters)

# Print iteration vs J

plt.plot(range(iters), betas[:, -1])

plt.xlabel('iteration')

plt.ylabel('J(beta)')

Aparently the cost function is not converging

Lets change alpha and increase the number of iterations

beta_ini = np.array([0., 0., 0.])

alpha = 0.5

iters = 1000

betas = gradient_descent(X_, y, beta_ini, alpha, iters)

# Print iteration vs J

plt.plot(range(iters), betas[:, -1])

plt.xlabel('iteration')

plt.ylabel('J(beta)')

print('betas using gradient descent\n', betas[-1, :-1])

Using the normal equations¶

betas_ols = np.dot(np.linalg.inv(np.dot(X_.T, X_)),np.dot(X_.T, y))

betas_ols

Difference

betas_ols - betas[-1, :-1]

x = np.array([3000., 3000.**2])

# scale

x_scaled = ss.transform(x.reshape(1, -1))

x_ = np.c_[1, x_scaled]

x_

y_pred = lr_h(betas_ols, x_)

y_pred

y_pred = y_pred * y_std + y_mean

y_pred

Using sklearn¶

from sklearn.linear_model import SGDRegressor

from sklearn.linear_model import LinearRegression

clf1 = LinearRegression()

clf2 = SGDRegressor(n_iter=10000)

When using sklearn there is no need to create the intercept

Also sklearn works with pandas

clf1.fit(data[['area', 'area2']], data[' price'])

clf2.fit(X, y)

Making predictions

clf1.predict(x.reshape(1, -1))

clf2.predict(x_scaled.reshape(1, -1)) * y_std + y_mean

Evaluation metrics for regression problems¶

Evaluation metrics for classification problems, such as accuracy, are not useful for regression problems. We need evaluation metrics designed for comparing continuous values.

Here are three common evaluation metrics for regression problems:

Mean Absolute Error (MAE) is the mean of the absolute value of the errors:

$$\frac 1n\sum_{i=1}^n|y_i-\hat{y}_i|$$Mean Squared Error (MSE) is the mean of the squared errors:

$$\frac 1n\sum_{i=1}^n(y_i-\hat{y}_i)^2$$Root Mean Squared Error (RMSE) is the square root of the mean of the squared errors:

$$\sqrt{\frac 1n\sum_{i=1}^n(y_i-\hat{y}_i)^2}$$y_pred = clf1.predict(data[['area', 'area2']])

from sklearn import metrics

import numpy as np

print('MAE:', metrics.mean_absolute_error(data[' price'], y_pred))

print('MSE:', metrics.mean_squared_error(data[' price'], y_pred))

print('RMSE:', np.sqrt(metrics.mean_squared_error(data[' price'], y_pred)))

Comparing these metrics:

- MAE is the easiest to understand, because it's the average error.

- MSE is more popular than MAE, because MSE "punishes" larger errors, which tends to be useful in the real world.

- RMSE is even more popular than MSE, because RMSE is interpretable in the "y" units.

All of these are loss functions, because we want to minimize them.

Comparing linear regression with other models¶

Advantages of linear regression:

- Simple to explain

- Highly interpretable

- Model training and prediction are fast

- No tuning is required (excluding regularization)

- Features don't need scaling

- Can perform well with a small number of observations

- Well-understood

Disadvantages of linear regression:

- Presumes a linear relationship between the features and the response

- Performance is (generally) not competitive with the best supervised learning methods due to high bias

- Can't automatically learn feature interactions